![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 41 (Issue 01) Year 2020. Page 25

VYSOCHAN, Oleg S. 1 & HYK, Vasyl V. 2

Received: 24/09/2019 • Approved: 11/01/2020 • Published 15/01/2020

ABSTRACT: The necessity of developing conceptual basis of forming accounting information in strategic cluster management has been grounded. The concept of accounting has been formulated on the basis of system approach: the place of accounting within strategic management information system has been defined; basic elements (aim, objectives, functions, subject, methods, tools), which constitute methodological basis of current accounting theory, have been conceptually specified and structured. |

RESUMEN: La necesidad de desarrollar una base conceptual para la formación de información contable en la gestión estratégica de conglomerados está demostrada. Basado en el enfoque sistemático, se forma el concepto de contabilidad: se determina el lugar de la contabilidad en el sistema de información de gestión estratégica; elementos básicos conceptualmente especificados y estructurados (propósito, tareas, funciones, materia, métodos, herramientas) que forman la base metodológica de la teoría contable moderna. |

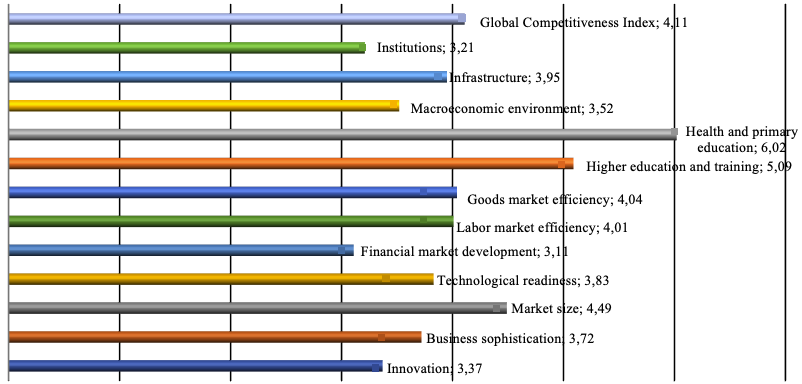

Taking into account the preparation process of Ukraine to join the European Union, matters of enhancing competitiveness of the national economy have become topical. The Global Competitiveness Report 2017-2018 -, issued by the World Economic Forum within Systemic initiative to shape future economic progress, cites country rating according to The Global Competitiveness Index, which consists of over 100 variables grouped into 12 benchmarks. According to research data, Ukraine takes 81st place among 137 countries in the world and has worsen its positions comparing with the previous period by 4 out of 12 main indicators (fig. 1).

Fig. 1

The Value of the Global Competitiveness

Index of Ukraine in 2017-2018

Source: https://www.weforum.org/reports/the-global-competitiveness-report-2017-2018

In view of this, in conditions of deepening integration of Ukraine with the European Union the problem of improving infrastructure and organizational-economic mechanisms, which will facilitate cooperation, is topical for innovative development of the national economy.

Traditional tools of its development do not fully meet new conditions of management, challenges of the environment and do not allow us to solve the problem of competitiveness of domestic enterprises on the world market. One of the effective mechanisms to stimulate the development of regional economy is transition to cluster model. Nowadays cluster is an organizational and managerial form and form of integration and cooperation and a means of ensuring the competitiveness of regional economic development. Formation and establishment of effective interaction demands deep understanding of economic essence of the processes of clustering Ukrainian economy.

It is worth mentioning that in EU countries cluster policy and development of innovative cluster initiatives are carried out by certain organization, mainly Europe INNOVA, The European Cluster Observatory, PRO INNO Europe, European Cluster Alliance. One of the most in-depth research of European cluster initiatives (data of 356 cluster organizations from 50 countries of the world was used) was indicated in The Cluster Initiative Greenbook 2.0 [(The Cluster Initiative Greenbook 2.0)], special attention was paid to the matters of organization, management and financing of cluster formations.

Considering the experience of European countries, more and more enterprises in Ukraine are undergoing an informal clustering stage. Consequently, there appears an objective need to develop information support of cluster management which demands a significant review of the role and importance of accounting system as an effective factor in meeting information needs.

Methodological basis of the research consists of a set of dialectical methods, the latest views and scientific thesis of leading scholars concerning accounting. The study is based on system approach which became the basis for formation of accounting in strategic cluster management.

To accomplish the assigned task, such methods and technics as analysis, synthesis, induction, deduction, generalization, system-structural have been used in order to form and develop accounting conceptual provisions in strategic cluster management.

The informational basis of the research comprises scientific sources (articles, materials of scientific and practical conferences), the Internet sources and results of researchers made personally by the author.

In modern conditions of economic environment, the system of cluster management requires the use of brand new approaches to form development strategy and make management decisions. Management effectiveness is highly dependent on information provision within which an important place belongs to the accounting system. Globalization of economic processes and dynamics of external environment predetermine the necessity to create strategy-oriented accounting. The necessity of creating accounting information for strategic purposes of cluster management is emphasized by some researchers.

Pylypenko A. A. put forward the hypothesis of appropriateness of extending the accounting process by adding signs of perspective to financial accounts (ensures its transformation into strategic accounting) and subordination of cluster development to the condition of maximizing its competitive potential (cluster’s potential here is the object of accounting observation). It is offered to manage cluster development by taking into consideration the principle of reflection since interaction of cluster members can be identified as “information management” (terminology by T. A. Taran), when one cluster member transfers the basis for the decision to the other (it is quite obvious that such basis must be based on accounting data with their certain transformation) [(Pylypenko, 2012)].

In M. Drohomyretskyy’s opinion, accounting and analytical support of cluster management systems in the agricultural sector of economy should be formed gradually; but in this context the analysis of information needs, taking into consideration specifics of business processes of agricultural organizations, becomes important. The attention should be paid to the fact that in huge agricultural organizations in order to form strategic information a corresponding monitoring system must be created, and strategic accounting can be used within management accounting [(Drogomyretska, 2015)].

Thereby, to sum up, we may state that cluster unions have the task of forming and effective functioning of accounting and information support of the strategic management system. Accounting data as a constituent part of information support are significant to management so that to plan and predict financial condition of certain members and the whole integrated structure. It should be noted that accounting system of an individual cluster member is the information flow integrator and key component of the complex accounting system.

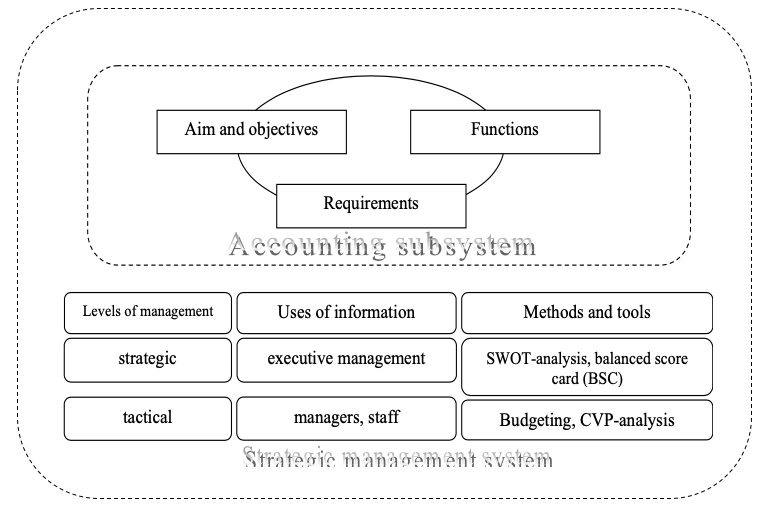

In order to form the complete picture of accounting it is important to form and identify the organized set of interconnected system-forming elements which form its conceptual basis and mechanism of practical implementation aimed at achieving aims of subject-object relations and information support for the implementation of strategic goals of the cluster. Such structure-forming components of accounting include the aim, objectives, functions, requirements, methods and tools. Taking the above mentioned into consideration, we suggest the conceptual approach to form accounting information in strategic cluster management (fig. 2), which defines the basics of building-up and maintenance of accounting records and constitutes its theoretical and methodological basis.

Fig. 2

The conceptual approach to form accounting information

in strategic cluster management

Source: formed by the author

The main aim of accounting in strategic cluster management is focused on presentation of regularity and systemic formation of strategically relevant information. The stated formulation defines main objectives of accounting. However, in modern accounting system in the cluster there appear objectives which cannot be performed fully by traditional tools which call for their transformation. “Paradigmatic development of accounting indicates that the given system faces objectives which are modified at each historic period. Talking about the characteristics of modern paradigm of accounting development, we may conclude that, besides modification of objectives, complete reorientation of accounting occurs and new objectives appear conditioned not only by reorientation to a new user but also by transformation of motives and, respectively, requests of all participants of business relations interested in the accounting information” [(Grytsyshen, 2015)].

To A. A. Osmonova’s mind, the objective of integrated cluster accounting system of agricultural sphere of economy is to streamline information flows, minimize the amount of primary information by reducing its duplication, provide effective access to information resources of enterprises that are a part of agrocluster, managers of all levels so that to make motivated management decisions [(Osmonova, 2014)].

O. S. Vysochan, describing characteristics and peculiarities of accounting cluster, indicates that it “must provide useful information to enterprises – cluster participants concerning reduction of expenses per unit of output through joint activities along with increasing of demand for it; increase of innovation activity through the occurrence of overflow of innovation; improving the efficiency of financial and material resources; activation of investment processes; raising of social standards for staff etc.” [(Vysochan, 2016)].

While forming the accounting objectives, it is necessary to take into consideration the fact that cluster management system is very complex, thus it should generate information based on user requests at different hierarchy levels:

– at the higher level – based on degree of achievement of a strategic aim of organizational structure activity;

– at the lower level – based on degree of achievement of a strategic aim of each participant of the structure.

It is significant to indicate that the objective of accounting in cluster is not only to register facts of economic life for the purpose of providing information to interested users, but also be aimed at increasing competitiveness of economic development of the region and the country as a whole.

Accounting in cluster as an integrator of information flows, besides conventional, must ensure implementation of the following objectives:

- facilitate coordination between participants and must become the information basis for development of tactics and strategies for the development of the union;

- facilitate display of characteristics and accounting objects specific to the cluster (contributions of participants, internal calculations, transaction costs, costs of innovation);

- identify and evaluate reserves and non-financial factors which significantly affect the development of the union;

- form the informational basis for planning, forecasting, analysis and control of cluster financial and economic activity.

Solving the mentioned accounting objectives will ensure the achievement of the goal to form complete, reliable and relevant information for effective management and will play a significant role in the harmonious development of the cluster. The suggested objectives will expand the purpose of accounting system in ensuring the execution of functions. Since accounting is an information component of cluster management, it must perform a number of functions derived from management functions: planning, forecasting, analytical, control, communication and coordination. However, the main function of accounting in strategic cluster management should be information support of long-term management decisions.

The implementation of abovementioned accounting objectives is ensured by compliance with requirements to accounting information: relevance, comparability, timeliness, integrity, reliability, materiality, relevance, significance.

An important feature of strategic management in cluster is that the object of governance is the joint activity of independently interacting economic entities, each of which performs its functions in an integrated structure. Therefore, accounting in the cluster should help coordinate the relationships between participants and must become an information basis for the development of tactics and strategies for the development of the union. The tactical level of cluster management is a set of management structures of individual participants, each of which independently chooses decisions and the way of their implementation from alternative options. The strategic level of management should be represented by the structure in which the cluster acts as a management object as a coherent organizational system.

Each economic entity creates specific methodological tools that provide substantiation, control of implementation and evaluation of the effectiveness of management decisions. An important role of management tools lies in the fact that it determines the form and mechanism of accounting system functioning in practice and the nature of interaction of its various levels. The strategic level of cluster management can be used by matrix tools, mainly SWOT-analysis and balanced score card (BSC), and at the tactic level – budgeting, CVP-analysis etc.

From a potential perspective, in our opinion, there are such significant tools as a balanced score card and budgeting system which penetrate all levels of management – from the strategic to operational, solve the largest number of accounting objectives, provide a systematic description of the cluster activity and are closed loop feedback techniques (accounting and analytic support for the management process at all stages). Combining these tools into a single information model to support decision-making and implementation of management decisions allows us to calculate synergetic effect of their interaction, increasing the ability to achieve goals.

The concept is the basis to form accounting system and should provide interested users with information on general approaches to organizing and maintaining accounting in the cluster. Accounting in strategic cluster management can be defined as an organizational and information system for supporting managerial decisions with strategic focus. Since strategic insight is focused not so much on retrospective but on perspective estimates, the value of accounting information becomes bigger in volume and nature. This leads to the emergence of techniques and procedures which were not used in traditional accounting but have become needed at the strategic management level.

A characteristic feature of accounting is availability of regular information support for the strategic decision-making process. The essence of accounting information in strategic cluster management can be reduced to three main positions:

1. Accounting is a system of collecting and grouping necessary (relevant) information.

2. Accounting information is both financial and non-financial in nature, and its assessment and measurement may be performed differently.

3. The formation and use of accounting information in strategic management comes primarily from utilitarian standpoint of the need to achieve certain strategic goals.

(n.d.). Retrieved from The Global Competitiveness Report 2017-2018: http://www3.weforum.org/docs/GCR2017-2018/05FullReport/TheGlobalCompetitivenessReport2017%E2%80%932018.pdf

Drogomyretska. (2015). Accounting, Control and cnalysis in the conditions of institutional change and sustainable economic development: materials of International scientific and practical internet conference. Accounting and analytical support for the management system in cluster formations of the agrarian sector of economy, (pp. 57-59).

Grytsyshen, D. A. (2015). Transformation of accounting tasks as a basis for the development of its theoretical and methodological design. Scientific bulletin of the international humanities university. Series: Economics and management (11), pp. 280-286.

Osmonova, A. A. (2014). Management accounting in cluster formations of agrarian sector. Bishkek.

Pylypenko, A. A. (2012). Consolidation of accounting information in the reflexive management of the development of competitive potential of the tourist and recreational cluster. BusinessInform , pp. 48-51.

The Cluster Initiative Greenbook 2.0. (n.d.). Retrieved from https://www.clusterportal-bw.de/downloads/publikation/Publikationen /download/dokument/the-cluster-initiative-greenbook-20/

Vysochan, O. S. (2016). The concept of cluster accounting: characteristics and features. Accounting and finance (1(71)), pp. 15-21.

1. Doctor of Science in Economics, professor of the Department of accounting and analysis. Lviv Polytechnic National University, Ukraine. E-mail: Vysochan_oleg@ukr.net

2. PhD in Economics, associate professor of the Department of accounting and analysis. Lviv Polytechnic National University, Ukraine. E-mail: Vasiahyk@ukr.net

[Index]

revistaespacios.com

This work is under a Creative Commons Attribution-

NonCommercial 4.0 International License