![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (Number 12) Year 2018. Page 26

Vol. 39 (Number 12) Year 2018. Page 26

Zaida А. ILIMZHANOVA 1; Venera R. BURNASHEVA 2; Barkhudar Sh. GUSSENOV 3;

Received: 23/12/2017 • Approved:22/01/2018

ABSTRACT: The paper examines the significance of efficiency of interaction between taxpayers and state authorities in the Republic of Kazakhstan, which depends on the optimization of business processes and successful implementation of well-known world market tools in the management processes of state revenue authorities. Combined fiscal functions of tax and customs bodies with addition of functions in the sphere of counteracting economic crimes will help to reduce administrative barriers for businesses and improve tax collection. |

RESUMEN: El documento examina la importancia de la eficiencia de la interacción entre los contribuyentes y las autoridades estatales en la República de Kazajstán, que depende de la optimización de los procesos comerciales y la implementación exitosa de las conocidas herramientas del mercado mundial en los procesos de gestión de las autoridades de ingresos estatales. Las funciones fiscales combinadas de los organismos tributarios y aduaneros con la adición de funciones en la esfera de contrarrestar los delitos económicos ayudarán a reducir las barreras administrativas para las empresas y mejorar la recaudación de impuestos. |

Evolution of Kazakhstan taxation at the sixth (modern) stage is characterized by introduction of standardization and regulation of public services in management activities. The main goal is to study the system of management processes for optimization of fiscal authorities in Kazakhstan in order to reduce administrative barriers and create trustful relationships with taxpayers. Expected results of improving management processes, including business processes, should not contradict the concept of “service” state for business and population. At the same time, they should contribute to unconditional execution of tax liabilities by taxpayers through fiscal functions of tax administration.

The presented below SWOT-analysis of key management processes in the fiscal authorities of the Republic of Kazakhstan (RK) demonstrates the decisions, made by the Government of country in this sphere.

Table 1

SWOT-analysis of genesis of management processes in the organs

of state revenues of the Republic of Kazakhstan, authoring.

S (strength)

|

W (weakness)

|

O (opportunity)

|

T (threat)

|

In development and improvement of tax system, the key role is assigned to the departments of state revenues, as they are the driving force for reforming and application of tax and customs legislation, improving the quality of public services and adequate improvement of business processes (B. Gussenov, 2015).

In the process of the study were used General methods of research: methods of analysis of financial statements: horizontal, vertical, ratio, comparison, and other.

To study the tax system of Kazakhstan were used General scientific and special research methods:

- review of the regulatory framework;

- analytical method;

- economic-mathematical calculations.

Today foreign experience of taxation is provided by activation of state tax management and adaptation of functions to the peculiarities of development of a country.

For example, in the USA the control over timeliness of tax calculation and payment is assigned to the Internal Revenue Service of the Ministry of Finance (IRS). Taxpayers can make tax calculation by themselves or charge this procedure to the IRS with very short notice.

The system of penalties for tax offences is relatively fundamental in nature, involving fines, penalties and litigation (Markov et al., 2010).

In the UK, state fiscal management is assigned to the Treasury, which is implementing economic policies along with the Inland Revenue Department and Department of Customs and Excise. Thus, municipalities have the right to set taxes for local purposes.

Thus, in the countries with advanced economies we can observe the prevailing trend for calculation and optimization of taxes by professional consulting and auditing companies, which is practically a preventive form of control for executing tax liabilities (Abayev, 2015).

Corporate tax management focuses on optimizing the procedure of calculation and payment of taxes by means of using the favorable opportunities of current legislation. However, there is always dilemma for honest taxpayers in choosing correct positions within behavior as a part of business reputation.

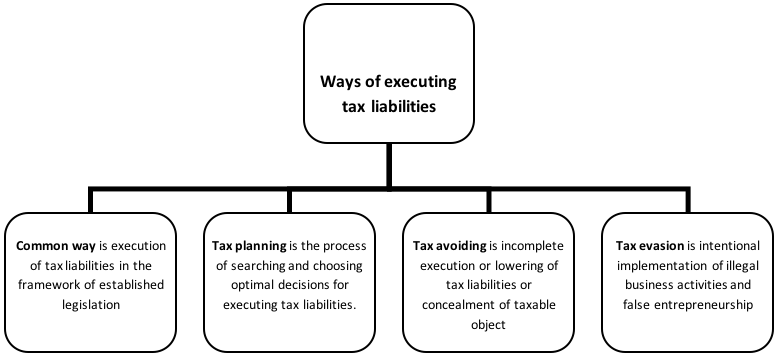

Scheme 1

Ways of executing tax liabilities, authoring

It is relevant to study the second method or phase-optimization of tax liabilities and balance management processes.

Phasing of planning is to choose: stage 1 – preferential tax treatment; stage 2 –location of object and activity; stage 3 - legal status; stage 4 - analysis of taxation elements; stage 5 –market perspectives (tenders, grants, subcontracting); stage 6 – model of production (shop floor) management; stage 7 – management decisions (Glauberman, 2011).

The need to adapt known business processes to the specifics of tax system should correspond to the priorities of fiscal policy at every stage of historical development of the country. This is one of the most important theoretical approaches in the solution of this problem. The growing role of taxes in the course of the past century demanded a new perception of their place in economic theory (Ilimzhanova, 2016). The main starting point was the premise that the system of market relations are imperfect and not very adjustable. In the most concentrated form these provisions have been formulated by English scientist Dzh. M. Keynes, the founder of the modern system of government system of regulation. According to his theory of employment, interest and money, the maximum economic growth can provide only the intervention of the state. The effectiveness of this regulation was determined by the ability of raising funds for investment, the achievement of full employment and the prospect of reducing interest rates on loans through the use of taxes as a “built-in stabilizers” of the economy. In a recession that has included reduction of taxes, providing many different incentives to increase investment activity. In the phase of economic recovery was proposed curtailment preferences, higher taxes to curb economic growth and prevent the onset of the crisis of overproduction. Not less significant scientific merit John. M. Keynes should be considered as the development of the neoclassical interpretation of taxes. In his opinion, the public needs should be considered indivisible wider collective, in the form of exclusively public purposes. Considering the weak private investment controller, he offered them to actively complement the investments from the budget due to tax revenues through the multiplier effect would increase employment and national income growth. Source: http://5fan.ru/wievjob.php?id=97448

If public governance faces the problem of making such managerial decisions, which contribute to the most comprehensive mobilization of tax revenues to the budget, in accordance with tax legislation, challenge for tax management of enterprises is to lessen payments and minimize of tax payments to the budget in accordance with tax legislation (Tax Code, 2008).

In 2016, the state revenue Committee begins the implementation of the pilot project of horizontal monitoring on example of tax administration in the Netherlands. The concept of horizontal monitoring means "fewer rules, better enforcement of legal rules and greater accountability on the part of society".

The monitoring of apriori - confidence, enabling mutual exchange of information between tax administrations and taxpayers, including electronic format, prevention and elimination of economic risks. The expectation from the methods of horizontal monitoring – reduce the number of cases of tax evasion (D. E. Ergozhin, 2016).

Planned changes to the Tax Code regarding the procedure for conducting tax monitoring and transfer to new control model in 2017 for about 300 large enterprises in the country. The implementation of E - auditing on the basis of the positive international experience allows to reduce the period of inspection and related costs (the Committee of state revenues of the Ministry of Finance of the Republic of Kazakhstan //Electronic resource.-03.12.2015.- www.kazinform.kz.)

Reorganization of tax management through merging of all the financial authorities into the State Revenue Committee of the Ministry of Finance of the Republic of Kazakhstan took place over a year ago (Ilimzhanova, 2016).

State revenue authorities are state bodies, which provide tax receipts, customs duties and other obligatory payments to the budget, implement customs affairs in the Republic of Kazakhstan, exercise powers for prevention, identification, preclusion, disclosing and investigation of crimes and offences, referred to the jurisdiction of this body by the laws of the Republic of Kazakhstan, and perform other powers, provided by the legislation of the Republic of Kazakhstan (Code of the Republic of Kazakhstan “On taxes and other obligatory payments to the budget”, 2016).

The organizational structure of Committee is divided into separate units with corresponding functions. This is the well-known process in management of departmentalization or functional specialization. The idea of management hierarchy together with departmentalization is the basis for creating the State Revenue Committee with a hierarchical type of structure. The structure is almost a demonstration of linear-functional organization of management with “mine” principle of structure (management of financial offences, customs administration, appeals, etc.). Hierarchy of service (“mine”) is top-down or forms scalar management chains. In this case, scalar management chain shows all the “floors” of management levels through delegation of authorities to the subordinate units not only in the central administration (subdivisions of departments), but also in the subordinate territorial units, which allows to coordinate joint work of organization vertically.

The element of linear and staff structure of management is availability of staff-on duty part of services of economic investigations (Tengrinews, 2015).

As a result, the Establishment of the Committee of State Revenues was reduced administrative barriers. It means that instead of some control agencies for road crossings there are only border services and state revenue authorities with functions of customs (including radiation), transport, sanitary-quarantine, veterinary, phytosanitary and export control.

When you export, you need to provide 3 documents instead of 10, when you import - 4 instead of 12. Work on electronic submission of customs declarations, using digital signatures, has been completed. A participant of foreign trade activities can receive background information on customs tariffs, defining code of commodity nomenclature, duty rates and list of permits free of charge. The “green corridor” is developed for bona fide participants of foreign economic activity, in the respect of which simplified procedures of customs inspection are applied (Ministry of Finance, 2015).

This managerial decision is made at the level of Central Apparatus of State Revenue Committee together with the Investment Committee of Ministry of Investment and Development of the Republic of Kazakhstan: a special mode is being implemented by the principle of “green corridor”, i.e. the State Revenue Committee will administer investors who concluded contracts with the Investment Committee directly for reducing terms of examination, design, execution of tax liabilities (Speech of the State Revenue Committee Chairman D.Yergozhin at the extended meeting of Political Council of “Nur Otan” Party - Electronic resource: http://kgd.gov.kz).

This decision is made within the framework of corporate governance reform, recommended by OECD, in order to create favorable investment atmosphere.

As a result of systematic introducing new approaches in management by the indicator “burden of customs procedures”, Kazakhstan rose to 55th position, which is higher than the last year position by 22-points.

In comments, National Analytic Centre of Nazarbayev University noted that 73 indicators of 114 of Global Competitiveness Index are improved, 30 indicators are lowered, there are no changes in 11 indicators, 5 indicators have improved ranking by 20 positions. This is the best ranking results in the country’s history ( Kazakhstan improved its positions in the ranking Global Competitiveness Index -Electronic resource:https://tengrinews.kz/kazakhstan_news/kazahstan-uluchshil-pozitsii-eytinge-globalnoy-282353//2015/10/14/ ).

By the time of writing the article, revenues of state budget for 9 months of 2015 has been performed on 100.3% (plan – 3 179 billion KZT, fact – 3 187 billion KZT, exceeding – 8 billion KZT); in the part of local budget, the plan is executed on 102.4% (plan - 1 092 billion KZT, fact – 1 119 billion KZT, exceeding – 27 billion KZT); in the part of the Republican budget execution was 99.1% (plan – 2 087 billion KZT, fact – 2 069 billion KZT, non-fulfillment – 18 billion KZT). It should also be noted the decrease in the level of arrears, as for October 1, it decreased by 19.3% or 22.6 billion KZT, so the arrears were $ 94.9 billion KZT (Ministry of Finance, 2015).

What has been achieved is the result of increased voluntary payment of taxes and other obligatory payments to the budget (Report materials of the expanded Board of the Ministry of Finance of the Republic of Kazakhstan. - Electronic resource: http://newskaz.ru//economy20151102/10114713 ).

The Economic Investigations Service of State Revenue Committee has achieved certain results: 8 377 criminal cases are registered. The amount of damages in criminal case amounted to 67.7 billion KZT; it is on 36% more than in the same period in 2014 it was 49.7 billion KZT, including reimbursed damage for 32.8 billion KZT, which is 1.7 times more than last year – 18.8 billion KZT. In order to ensure compensation for the caused damage, property in the amount of 8.7 billion KZT was seized, while during the first 9 months of 2014 this figure amounted to 3.5 billion KZT, i.e. increased by 2.5 times. The recoverability of damage, taking into account the arrested property, amounted to 61.5% against 44.8% in the last year.

Economic Investigations Service actively applies Risk Management System for filtering potential of pseudo-enterprises in the initial stages of their work. So, in 2015 pre-trial investigation is initiated in respect of 1 922 pseudo-enterprises, 343 claims for recognition of registration of pseudo-enterprises and their transactions invalid are introduced in the court. 370 criminal offences were identified in the amount of about 4 billion KZT in the field of public procurement with 100% refund (Burnasheva, 2016).

In the sphere of customs 2.9 billion KZT are compensated for damages, property for the sum of 1.4 billion KZT is arrested within 269 criminal cases. Operations of 11 underground shops for alcoholic beverages are stopped, 6.6 million of fake accounting and control marks and 6.3 million bottles of hidden alcohol are seized in the total volume of 186 thousand alcohol (The briefing materials of economic researches of the State Revenues Committee of the Ministry of Finance of the Republic of Kazakhstan dated 05.11.2015-Electronic resource: http://www.inform.kz/).

By 2016 modernization of customs inspection for 11 car posts on the border with China will have been expected with the increase in speed of examination by 4 times and increase of revenues to the budget income by 30%-50%. The project on modernization of tax service will have been completed, within the framework of which automating the process of electronic invoicing with new system of goods and transport waybills is being implemented for accounting of turnover in the country and reduction of shadow economy (Official website of the TV Channel Khabar, 2015).

Management processes in the fiscal authorities are closely interconnected with regulation of interpersonal and intergroup relationships, especially with consumers of public services. In this regard, a number of subsidiary legal acts have been adopted, including the “Code of professional ethics for employees of tax service bodies of the Republic of Kazakhstan” by the Order of Tax Committee Chairman of the Ministry of Finance of the Republic of Kazakhstan No. 47 dated 30.09.2006 and “Code of corporate behavior of employees of tax service bodies of the Republic of Kazakhstan” by the Order of Tax Committee Chairman of the Ministry of Finance of the Republic of Kazakhstan No. 910 dated 6.12.2007 (Ministry of Finance, 2014).

For the first time in the taxation history of Kazakhstan, the Taxpayer Charter of the Republic of Kazakhstan had been developed and approved (Order of Tax Committee Chairman of the Ministry of Finance of the Republic of Kazakhstan No. 472 dated 29.09.2006) (Burnasheva, 2016).

The ability to form the favorable moral and psychological atmosphere, constant quality improvement of rendered public services to taxpayers by subordinates; ability to set long-term and short-term goals and objectives to subordinates, and not to shift off responsibility for decisions to subordinates (Rules of ethics for state employees of the Ministry of Finance of the Republic of Kazakhstan, approved by the Order of the Deputy Prime Minister of the Republic of Kazakhstan,2014).

Execution of the Law of the Republic of Kazakhstan “On public services” No. 88-V dated 15 April 2013 (amended on 29.09.2014) has almost become the part of management process in the fiscal authorities (Law of the Republic of Kazakhstan “On public services”, 2013).

In order that the consumer will receive a quality service, for government an important re-engineering of business processes, which involves the fundamental rethinking and radical redesign of business processes to achieve high results in the field of management (Akorda, 2013).

International experience of tax administration was studied on the example of Finland, Singapore, Netherlands, Lithuania, and Norway. The cost of collecting one unit of taxes in Denmark is 0,67%, Germany – 0,79%, Singapore 0.8 per cent. In Kazakhstan, this figure is 9.6 billion or 0.96 percent of total budget revenues. (The Chairman of the RTC Dzhumadildayev A. S. reforming the tax administration. Proceedings of the VII Astana economic Forum. Session "Innovative approaches to managing business processes in tax administrations".- Astana, 22 may 2014.)

Set By The President Of The Republic Of Kazakhstan N. Nazarbayev, in terms of the Nation – 100 concrete steps on implementation of five institutional reforms task in a permanent reduction of transaction costs of functioning of economy to the state institutions of governance should be resolved by the introduction to the theory and practice of tax management recognized by science successful management tools like Lean management, Kaizen management, CAF and others (The concept of reengineering of the tax business processes.-Astana, 2013).

The entry of Kazakhstan into the Customs Union and the common economic space, Eurasian economic Union, the world trade organization marked a qualitatively new integration processes in taxation. Is the actual implementation of the OECD principles of corporate governance in the business sector and the management of the integration of global processes (VII Astana economic Forum, 2014).

Main focus is on the process of improving activities of fiscal authorities, i.e. any problem can be resolved only in the place of its origin, realizing its inner nature, cause; this can be achieved by improving the effectiveness of self-development (Markov, Rabunets, 2010).

It indicates employees’ desire for successful joint activity with taxpayers or application of core postulate of Kaizen theory for continuous improving processes.

Methods of management, taken from business environment, contribute to lowering the cost of providing tax income. In particular, these methods include LEAN management, or lean production, involving all the employees and maximum customer orientation as well as reduction of comprehensive costs and losses in the process of optimizing business processes (Ilimjanova et al., 2016).

Based on the opinions of Bekbosynova A., for the tax policy of countries which have a long-term concept of the national economy, characterized by the following features: a Clear definition of the problems facing the country's economy; Ranking of goals according to their degree of importance and focus on achieving the most important ones; the analysis and study of foreign experience of tax reforms, a clear understanding of economic results, benefits and losses in the implementation of each of the reform programs; evaluate the effectiveness of implementation of such programs in the past; Analysis of available tools; baseline Analysis; Adjustment policies, taking into account national specificities point in time. Spending tax policy, its subjects can affect the economic interest of the taxpayers to create such conditions for their management that are most beneficial for the taxpayers and for the economy as a whole. Source: http://5fan.ru/wievjob.php?id=97448

Effective in improving the process efficiency is practice of applying benchmarking methods, involving open access to information. Kazakhstan businesses and entrepreneurship are aware of the potential of information resources of State Revenue Committee in making their business decisions: http://kgd.gov.kz, www.adilet.gov.kz/ru, www.adilet.gov.kz/ru/kisa/zapret . (Gussenov, 2016)

Expanding the use of benchmarking in Kazakhstan should be the establishment of infrastructure between all the state bodies, fixing commercial transactions (State Revenue Committee, notary office, licensor, Road traffic police, Centers of real estate appraisal, Committee on land management).

Considerable importance of LEAN management is in public services. In Kazakhstan reducing non-production costs, saving time, funds of individuals and businesses are being carried out in the development of activities of Public Service Centers (PSC) and e-government. Thus, this saving should include the reduction of unnecessary functions, associated with the creation of customer value in all the spheres of economy (Abayev,2015).

Glauberman A. figuratively describes the atmosphere of LEAN management in the article “Three-layer cake of LEAN-management”: “... it is in the form of a three-layer cake. Its basis is learning, the middle layer is consulting or support, the top layer is coaching or mentoring, these are three elements which comprise the process” (Glauberman,2011).

Training in the state revenue authorities is system-related. Taxpayers and staff participate in the training courses and tax seminars, conferences, round tables, forums, etc. Process consulting is fully dedicated to queries, questions, requests, problems of taxpayers, so a group of employees need to find their solution.

Coaching or mentoring is regulated by the Rules of fixing mentors for individuals, who have been hired in an administrative public office for the first-time, according to the Chairman Order of RK Agency on Public Service Affairs dated September 18, 2013, No.06-7/148 for experience transfer, forming abilities and skills from more experienced employees to employees newly entering public service (Burnasheva, 2016).

Progressive reforming of taxation system in the Republic of Kazakhstan, in particular control systems has undoubtedly enriched not only the theory and practice of taxation, but by this moment it has reached a new level of harmonization of controlling fiscal authorities: tax and customs sphere and Economic Investigations Service.

Institutional changes in the field of taxation associated with the development of the tax system of Kazakhstan economy took place in the framework of three stages of tax reform:

The first phase of tax reform (from 1992 to June 1995) - phase of the new tax system of Kazakhstan based on the law "On tax system in the Republic of Kazakhstan", adopted on 24 December 1991. At this stage, were mainly used the experience of Russia and adopted a three-tier tax system which complies with the Federal structure of the state (national, state, local, and local taxes), but which did not correspond to a unitary state, which is Kazakhstan. During this period, the study of the development of the tax system and tax authorities engaged in such scientists as: G. Karagussova (taxes: the essence and practice of using - 1994), A.B. Zeinelgabdin (tax system - 1995), S. Babkina (new tax policy - 1995), B. Kadyrbekov (the basic principles of formation of tax system - 1995).

The second stage of the tax reform (from July of 1995 to 1999.) the stage of formation of a tax system adapted to the conditions of the country and conforming to international standards. From 1 July 1995. was promulgated the decree of the President of RK, having the force of law "On taxes and other obligatory payments to the budget" dated 24 April 1995. No. 2235. Was established two-tier tax system (national and local taxes). During this period, the establishment and improvement of tax management was studied by M. Esenbayev (towards a new tax system - 1996), M.T. Ospanov (tax management -1997), N.K. Mamyrov, Zh. Ikhdanov (state regulation - 1998).

The third stage of tax reform (2000- at the present time) is associated with the development of a new Tax Code, adopted on 12 June 2001 and entered into force on 1 January 2002., with the beginning of economic growth, which is characterized by an increase in such macroeconomic indicators as gross domestic product, gross national product and gross national income. During this period, while establishing and improving taxation management, a significant contribution to the development of perspective in the field of tax system of Kazakhstan, the problem was studied by A.I. Khudyakov (tax law - 2001), V.D. Melnikov (management of tax system 2013), A. Paavonakho, A. Witt (tax administrations - 2014), D.Ye. Yergozhin (state revenue authorities - 2015) (Burnasheva et al., 2016).

Forming favorable investment atmosphere plays a key role in creating comfortable business environment for domestic entrepreneurs and foreign investors to attract new businesses in Kazakhstan. Trend of improving indicators of Kazakhstan in different international rankings gives hope for prosperous future in solving this complicated problem by the state, including fiscal authorities, applying modern business technologies in management processes such as Kaizen, LEAN –management, benchmarking (Burnasheva, 2016).

Abayev D. (2015). In development mode //the Kazakhstan truth.-24 Nov.-No. 225(28101).-11p.

Code of the Republic of Kazakhstan "On taxes and other obligatory payments to the budget" (Tax Code) dated 10.12.2008.- No. 99.- IV as at 01.01.16 y.

Glauberman A. (2011). Three-layer cake lean management //Electronic resource - http://www.e-xecutive.ru

Gussenov B. S. (2015).Development of foreign economic activities in the age of globalization Tutorial LAP LAMBERT Academic Publishing, p. 316

Ilimjanova Z. A., Kaldiyarov D. A., Burnasheva V. R. (2016). Modern fiscal management of Kazakhstan.- Almaty: Economics.- 186p.

Kazakhstan has improved its positions in global competitiveness rankings /the Official website Tengrinews - https://tengrinews.kz/kazakhstan_news/kazahstan-uluchshil-pozitsii-reytinge-lobalnoy-282353//2015/10/14/

Kazakhstan will modernize customs points with China /the Official website of the TV Channel Khabar http://khabar.kz/archive/ru/ekonomika/item/36476-v-kazakhstane-provedut-modernizatsiyu-tamozhennykh-punktov-s-knr//22/10/2015

Markov V., P. Rabanes (2010). Kaizen is a long-term strategy of Japanese management. Heading Lean in Russia and the world.-11 Jun.- Electronic resource: http://www.leaninfo.ru/2010/09/24/lean-conference-gd/

The Chairman of the state revenue Committee Ergozhin D. E. at the enlarged meeting of the political Council of the party "Nur Otan" party / the Official website of the state revenue Committee of the Ministry of Finance of the Republic of Kazakhstan http://kgd.gov.kz (2016)

The Chairman of the RTC Dzhumadildayev A. S. reforming the tax administration. Proceedings of the VII Astana economic Forum. Session "Innovative approaches to managing business processes in tax administrations".- Astana, 22 may 2014.

The concept of reengineering of the tax business processes.-Astana, 2013.

The law of the Republic of Kazakhstan "On public services".- Astana: Akorda, April 15, 2013. - No. 88. – V3RK amended 29.09.2014y.

The materials of the report of the Board of the Ministry of Finance.-Electronic resource: http://newskaz.ru//economy 20151102/10114713 .

The materials of the report of the economic investigation Service of the state revenue Committee of the Ministry of Finance from 05.11.15-Electronic resource: http://www.inform.kz /

The rules of office ethics of state servants of the Ministry of Finance of the Republic of Kazakhstan, approved by order of the Deputy Prime Minister of the Republic of Kazakhstan – Minister of Finance of the Republic of Kazakhstan dated January 20, 2014 No. 16.

The state revenue Committee of the Ministry of Finance of the Republic of Kazakhstan //Electronic resource.-03.12.2015.- www.kazinform.kz

1. Taxes and taxation. Department of of Economics and service. Zhetysu state University named after I. Zhansugurov. The state revenue Committee. king_bara@mail.ru

2. Taxes and taxation. Department of Finance. Zhetysu state University named after I. Zhansugurov. The faculty of law and Economics. king_bara@mail.ru

3. Economic policy of the state. Department of public administration and management. Zhetysu state University named after I. Zhansugurov. The faculty of law and Economics. king_bara@mail.ru