![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 38 (Nº 62) Year 2017. Páge 2

Vol. 38 (Nº 62) Year 2017. Páge 2

Nataliya Evgenievna BONDARENKO 1; Tatiana Pavlovna MAKSIMOVA 2; Olga Aleksandrovna ZHDANOVA 3

Received: 06/10/2017 • Approved: 20/10/2017

ABSTRACT: In this paper, the authors address the possibility of implementing an alternative mechanism in the system of funding smaller forms of business within Russia’s agro-industrial complex – peer-to-peer (P2P) lending. The purpose of the research reported herein is to explore the characteristics of attracting financial resources via P2P lending and identify the potential for its use by smaller forms of business within Russia’s agro-industrial complex. The authors put forward the following scientific hypothesis: P2P lending can be used by smaller forms of business within the Russian agro-industrial complex to attract financial resources. To develop the above hypothesis, the authors undertook a number of objectives, resolving which produced the following inferences. In principle, P2P lending is no different from regular bank lending, but it has a few distinctive characteristics of its own: there are no traditional financial intermediaries involved, including banks; participants are natural and legal persons that are mainly small businesses and micro-companies; loans are extended at relatively low rates; deals are concluded mostly online; there is currently no separate legislative framework regulating Р2Р lending in Russia; some other factors. The authors propose a classification of auction-based Р2Р lending systems: an English auction, a Dutch auction, a closed auction for borrowers, a closed auction for lenders, and a joint-type closed auction. The paper identifies some of the factors that facilitate and those that impede the implementation of P2P lending in the system of funding smaller business entities within Russia’s agro-industrial complex. On the whole, despite some negative factors impeding the implementation of the above mechanism, right now there are really no insuperable barriers to its use by smaller forms of business, and, going forward, its strengths should only attract increasingly more participants interested in using additional financial resources. The authors are convinced their scientific hypothesis will be confirmed: P2P lending is going to help smaller forms of business within the Russian agro-industrial complex expand their potential for bringing in much needed financial resources on a short-term and mid-term basis at relatively low interest rates. |

RESUMEN: En este documento, los autores abordan la posibilidad de implementar un mecanismo alternativo en el sistema de financiación de formas más pequeñas de negocios dentro del complejo agroindustrial de Rusia: préstamos peer-to-peer (P2P). El propósito de la investigación informada en este documento es explorar las características de atraer recursos financieros mediante préstamos P2P e identificar el potencial para su uso por parte de pequeñas empresas dentro del complejo agroindustrial de Rusia. Los autores presentan la siguiente hipótesis científica: los préstamos P2P pueden ser utilizados por pequeñas empresas dentro del complejo agroindustrial ruso para atraer recursos financieros. Para desarrollar la hipótesis anterior, los autores llevaron a cabo una serie de objetivos, resolviendo lo que produjo las siguientes inferencias. En principio, los préstamos P2P no son diferentes de los préstamos bancarios regulares, pero tienen algunas características distintivas propias: no hay intermediarios financieros tradicionales involucrados, incluidos los bancos; los participantes son personas físicas y jurídicas que son principalmente pequeñas empresas y microempresas; los préstamos se extienden a tasas relativamente bajas; los tratos se concluyen principalmente en línea; actualmente no existe un marco legislativo separado que regule los préstamos de Р2Р en Rusia; algunos otros factores. Los autores proponen una clasificación de los sistemas de préstamo Р2Р basados en subastas: una subasta inglesa, una subasta holandesa, una subasta cerrada para prestatarios, una subasta cerrada para prestamistas y una subasta cerrada conjunta. El documento identifica algunos de los factores que facilitan y dificultan la implementación de préstamos P2P en el sistema de financiación de entidades comerciales más pequeñas dentro del complejo agroindustrial de Rusia. En general, a pesar de algunos factores negativos que impiden la implementación del mecanismo anterior, en este momento no existen barreras insuperables para su uso por parte de pequeñas empresas, y, en el futuro, sus puntos fuertes solo atraerán cada vez a más participantes interesados en utilizar recursos adicionales. recursos financieros. Los autores están convencidos de que su hipótesis científica se confirmará: los préstamos P2P ayudarán a las pequeñas empresas del complejo agroindustrial ruso a ampliar su potencial para atraer recursos financieros muy necesarios a corto y mediano plazo a relativamente bajas tasas de interés. |

Innovative forms of development of entrepreneurial and other types of activity both in Russia and around the world are signaling the need to transform the funding system, including based on the use of novel mechanisms for providing financial resources that are emerging today, which include hybrid forms of funding, like mezzanine financing and crowdfunding, which engages an unlimited number of people in the investment/lending process.

The issue of lending to smaller forms of business within the agro-industrial complex continues to be a major concern, despite sustained effort by the state. Banks are reluctant to lend to small business entities within the agro-industrial complex due to the often high levels of risk inherent to their operation, some of which is unpreventable (e.g., acts of God), while insurance premiums paid to have such risks insured are rather high, which makes it unadvisable to turn to insurers. Considering that the market is currently witnessing a clear-cut trend of lending institutions having their license revoked, the issue of access to financial resources for smaller forms of business within the agro-industrial complex is becoming an even greater concern. In this regard, the authors suggest exploring some alternative mechanisms for funding the activity of small business entities within the Russian agro-industrial complex, one of which is Р2Р lending. The purpose of this paper is to explore the characteristics of attracting financial resources via P2P lending and identify the potential for its use by smaller forms of business within the Russian agro-industrial complex.

Р2Р lending is not a totally novel mechanism in the Russian financial market, but its development is only just getting started in Russia, while in the US and countries of Western Europe this type of provision of financial resources is quite a common practice nowadays. For the most part, Р2Р lending implies a relationship between natural persons – it is quite rare to have P2P relationships between natural and legal persons, although there are no direct barriers to this and contractual relationships of this kind are possible. Of particular interest is the possibility and advisability of this kind of lending-investment relationships between natural persons and smaller forms of business within the agro-industrial complex. In addition to commercial gain in the form of interest on loans, natural persons can also reap social gains and get some moral satisfaction from funding one of the economy’s most significant sectors – the agro-industrial complex, which supplies the population with food. This kind of help may ensure that small business entities within the agro-industrial complex get the much-needed financial resources.

The authors put forward the following scientific hypothesis: the P2P lending mechanism can be employed by smaller forms of business within the Russian agro-industrial complex to bring in financial resources.

Substantiating the above hypothesis involves resolving the following 3 major objectives:

Once the objectives set for this study are resolved, its purpose will be regarded as achieved and the above hypothesis as confirmed.

The theoretical and methodological basis for this study is grounded in works and applied solutions by Russian and foreign scholars and practicians dealing with issues related to the area of the financial market as a whole (Mirkin, 2016; Slepov & Chalova, 2017) and the banking market in particular (Lavrushin, 2017; Larionova, 2017), the Р2Р lending market (Patlasov & Grakhov, 2016; Teteryatnikov, 2015; Mach, Carter, & Slattery, 2014), as well as the characteristics and ins and outs of the transformation of Russia’s agro-industrial complex by reference to the degree to which the sector is in demand in the minds of theoreticians and practicians (Gaisin, 2015; Maksimova & Bondarenko, 2017; Ustyuzhanina, 2016). The paper employs the dialectical method of enquiry, the systems approach, and a set of general scientific and special methods of research, including analysis (comparative analysis), synthesis, analogy, classification, as well as the historical and logical methods.

The paper’s information basis are certain foreign legal acts related to the area of the financial market and certain statutory and legal acts of the Russian Federation regulating the activity of banks, lending institutions, and microfinance organizations, the operation of platforms providing Р2Р lending services, the issue and circulation of securities, as well as the conclusion of various deals and effectuation of transactions related to them. In writing this paper, the authors relied on official statistical information, as well as information from the official websites of research agencies and institutions and other organizations.

P2P lending, also known as person-to-person lending, peer-to-peer investing, social lending, reciprocal lending, and peer lending, is about natural persons lending money to other natural persons, without the participation of entities that are traditional to the system of lending, like banks. Apart from natural persons, the Р2Р lending process may also involve sole entrepreneurs and legal persons, which, however, are mainly small businesses and micro-companies, since amounts involved in deals of this kind are normally not very big. Р2Р lending implies providing one with financial resources on a short-term or mid-term basis.

Technically speaking, the Р2Р lending mechanism is actualized via a special Internet platform, which, from the economic perspective, acts as a sort of marketplace where a buyer (borrower) meets up with a seller (lender). Furthermore, one and the same person may be a borrower and a lender. A perfect example of this kind of platform is WebMoney Transfer (WebMoney Transfer, 2017).

The Internet platform enables borrowers and lenders to locate each other and make a deal – i.e., it provides services related to the analysis of incoming requests for a match between each other. There is also the possibility of analysis of the financial reliability of the parties involved in the deal and verification of the deal’s integrity, which, however, depends on the capabilities of each particular P2P lending Internet platform, including whether or not it can provide all the relevant information.

It is especially worth noting that the basic Р2Р lending mechanism does not presuppose collecting money from investors with the promise that a certain amount of interest will be paid to them. The Internet platform is not a party to a deal, provides no guarantees that the terms of the loan agreement entered into by way of its mediation will be fulfilled, and provides no intermediary services related to servicing the debt, including in the way of transfer of funds between the parties involved. From the legal perspective, the Internet platform acts as a sole entrepreneur or legal person that provides intermediary services which are not subject to mandatory licensing. Here, the Internet platform generates its profit through commission fees, which may be established for either just borrowers or just lenders, or both. The platform will charge a fee for its services related to the search for counterparts to a deal.

It is worth noting that many Internet platforms positioning themselves as institutions providing services related to Р2Р lending are microfinance organizations listed in the state registry of microfinance organizations (Federal Law of the Russian Federation No. 151-FZ, 2010) and characterized by totally different principles of operation, expanded functions, and the capacity to handle a greater number of various types of deals. In Russia, such platforms include Loanberry and Вdebt.ru. In addition, it is worth noting that microfinance organizations meticulously check the creditworthiness of potential borrowers (especially, whether or not they own any real estate) and may generate not just fee revenue but also revenue from the difference between interest rates, which somewhat contradicts the primary essence of Р2Р lending, which presupposes getting a loan at a relatively low interest rate, notwithstanding the high levels of risk.

Deals in Р2Р lending are mainly concluded online, which requires the use of an electronic wallet and/or a bank card, as well as an electronic digital signature. The use of an electronic digital signature not only accelerates the procedure of concluding a deal but makes the process of servicing debts more transparent, straightforward, and reliable.

Documentation required of candidates for a loan may vary. Things like its comprehensiveness and having a qualified electronic digital signature may decisively affect the borrower’s rating and, as a consequence, the loan’s affordability – the maximum amount one may borrow and the minimum interest rate one may get, with most lenders tending to select counterparts in a rather meticulous manner.

Both lenders and borrowers have 24-hr access to their personal area on the Internet platform, which is quite a convenient feature that enables the maximum expansion of the geography of participants and working across long distances and different time zones.

The necessary amount of money the borrower wants to obtain via the Р2Р lending mechanism can be amassed from several lenders at once. That being said, a loan agreement will, normally, be entered into by each lender and borrower, i.e. a single loan will require several agreements substantiating it legally. By lending smaller amounts to different borrowers, each particular lender reduces their risks on the funds lent out and, consequently, has the ability to reduce the interest rate on the loan, even despite the fact that most loans are unsecured and deal participant checks are often minimal and just formal. In addition, it is worth noting another risk that is rather characteristic of the Р2Р lending mechanism: it attracts persons with a poor or non-existent credit history, which increases the risk that the loan will not be repaid. Risk management is more than restricted in Р2Р lending for lenders – essentially, it all comes down to just diversifying one’s loan portfolio.

Russia has yet to put in place a separate legislative framework regulating Р2Р lending, while in the US this type of service is regarded as a structural element in the securities market, which necessitates compliance with tougher requirements and fulfillment of certain obligations. This, no doubt, is intended to protect market participants and, above all, natural persons and other unqualified investors from unethical practices by counterparties. Be as it may, the Russian approach, predicated on the absence of special legislation on Р2Р lending, is pretty much justified, for this mechanism for extending financial resources can function as part of the nation’s general civil legislation that is already in place and operation, and there is a separate legislative framework in place for larger entities operating in an adjacent and pretty similar market – the microfinance market (Federal Law of the Russian Federation No. 151-FZ, 2010). Creating a special legislative framework for Р2Р lending may additionally complicate things across the legislative field, which is complex as it is.

The principal document regulating Р2Р lending in Russia is the Civil Code of the Russian Federation, more specifically its Part 2, which covers loan agreements (Civil Code of the Russian Federation: Part 2, 1996).

It is worth dwelling in some detail on the legal status of Р2Р lending. Pursuant to Russian legislation, loans may be extended only by banks or other lending institutions (Civil Code of the Russian Federation: Part 2, 1996), which immediately, regardless of the rest of the differences between loans and borrowings, bears testimony in support of Р2Р lending being, essentially, a relationship as part of a borrowing, rather than loan, agreement. From this standpoint, Р2Р lending may need to be termed Р2Р borrowing, but it is the term ‘Р2Р lending’ that has gained a firm foothold in business discourse, so the authors are going to use this particular term hereinafter, but the parties to a deal will be referred to as a borrower and a lender, which is in keeping with the discourse of Russia’s current regulatory and legal framework.

Apart from the main document regulating Р2Р lending, market participants may also want to resort to some other statutory and legal acts. These, for instance, may include the Federal Law of the Russian Federation ‘On Personal Data’, which obliges Internet platforms not to disclose confidential information and use it strictly within law. Confidential information here includes information from the personal area of users of an Internet platform, as well as some other data that may become accessible to the intermediary during the transactions.

In principle, Р2Р lending is no different from regular bank lending, as it is underpinned by the same principles: payment of reasonable interest, fixed schedule of repayment, and repayment. However, Р2Р lending lacks a proper focus on such principles as loan security and loan purpose.

Right now, the Russian market features Internet platforms that provide services related to Р2Р lending to everyone interested (e.g., WebMoney Transfer), but there may also be platforms intended for a limited circle of persons, entry into which is by invitation only.

To be in demand in the market, Р2Р lending is expected to offer some form of economic gain. As was noted above, an Internet platform receives commissions, but it is time now to also find out what, from the commercial point of view, makes Р2Р lending attractive to potential parties to a loan agreement.

A P2P lender can create an investment portfolio to generate a steady influx of revenue in the form of interest on loans extended – and with a relatively minor amount of risk based on robust diversification. Apart from this, here a lender not only preserves their capital but also makes additional profit off of it. When a lender provides financial resources to smaller forms of business within the agro-industrial complex, it is also about getting some moral satisfaction from funding one of the most vital sectors of the economy crucial to ensuring the nation’s food security.

A Р2Р borrower obtains financial resources at a lower interest rate than at a bank, even despite most loans being unsecured and a relatively sizable amount of risk for lenders. This is due to the fact that there are many lenders out there who are not after profit at any cost and may fund certain projects at lower interest rates just out of social considerations, and this may well be the case with projects within the agro-industrial complex. Also, as was noted above, a single loan may be extended by several persons, in which case it makes sense to arrange an auction, which will let borrowers choose from the most interesting propositions and help them get lower interest rates on loans.

Interest rates on Р2Р loans can be fixed or variable. Interest rates may vary based on a plethora of factors, including inflation, the key rate, reference securities market indices, and derivative financial instruments. It is possible to establish the minimum and maximum levels of the interest rate to protect the interests of both the borrower and the lender. The interest rate can be adjusted only within time periods stipulated in an agreement or in the event of certain circumstances arising as agreed upon and expressed in clear written form in an agreement as well.

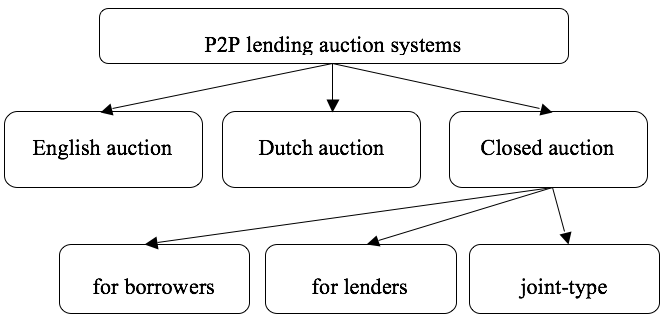

The interest rate on a loan may be established individually for each borrower and lender through negotiations based on the average interest rate there is at the time the agreement is signed or based on other indicators. It may also be determined through an auction. The authors propose the following way to classify the auction-based system of establishing the loan interest rate in Р2Р lending (Figure 1).

Figure 1

Classification of Р2Р lending auction systems

It is worth noting that the auction system can function only if a single deal will feature more than 1 participant from at least 1 of the parties.

The Р2Р lending mechanism is more accessible and flexible than bank lending, and may be regarded as advantageous for borrowers and lenders alike from both the commercial and non-commercial perspectives.

The implementation of Р2Р lending in the system of funding small business entities within the agro-industrial complex is impacted by a whole range of different factors. The authors deem it worth focusing only on the key factors underpinning Р2Р lending specifically and overlooking most of the geopolitical, general economic, etc., factors that impact the entire financial system as a whole.

Р2Р lending is mainly aimed at a short-term period. This characteristic may both repel and attract smaller forms of business within the agro-industrial complex.

On the one hand, some small business entities within the agro-industrial complex may need long-term financial resources to purchase machinery or an expensive facility. In that case, they are better off going to a bank, which will let them take out a loan secured by real estate, factor in all the ins and outs and conduct a thorough analysis of the company’s operation, and draw up a schedule for the repayment of the loan factoring in the seasonality of production, which is especially crucial to the operation of agricultural businesses. Р2Р lending is currently losing out to bank lending when it comes to funding large deals and taking out long-term loans.

On the other hand, smaller forms of business within the agro-industrial complex often need to fix cash gaps, acquire working assets with a rather quick turnover (e.g., certain varieties of seeds), as well as obtain financial resources in the event of unforeseen expenditure. In all these situations, it is possible to get a loan from a bank, but the interest rate will be real high, as there may be nothing substantial to secure against and risk levels are quite high considering the objectives toward which the funds are going to be used. In that case, one may be better off resorting to Р2Р lending.

It is also worth taking into account that to extend a loan banks are likely to require a standard, or possibly even extensive, set of documents, while in Р2Р lending lenders will only ask for a minimal amount of documentation. Considering the fact that smaller forms of business within the agro-industrial complex are often classified as sole entrepreneurs, micro-companies, or small businesses, which are known to face a plethora of special taxation and accounting regulations, these business entities are oftentimes unable to gather on time all the documentation required by the bank. Thus, for instance, pursuant to current Russian legislation (Decree of the Ministry of Finance of the Russian Federation No. 66n, 2010), small business entities are to submit their balance sheet report and profit and loss statement once a year at year end, which makes it quite problematic (in terms of time and labor expenditure) to submit those to the bank at a different time.

A factor that may impede the implementation of Р2Р lending in the system of funding within the agro-industrial complex is the issue of recovering debts from deal participants, with many, mainly natural persons, being reluctant to enter into a loan agreement for this very reason. Indeed, going to a collection agency may be quite costly, with some charging as much as 25% of the amount to be recovered and up, which is a really substantial loss for a particular natural or legal person representing a small business or a micro-company. Things are similar when it comes to pressing charges: court proceedings are costly and may take real long, which makes going to court economically irrational. It is pretty much impossible to do something major about the impact of said factor at the moment, so for the time being it will pretty much continue to affect the development of the financial system of Russia’s agro-industrial complex.

The fact that in its classic version the Р2Р lending Internet platform currently provides no services related to debt servicing may be a negative factor for certain borrowers and lenders and may impede the implementation of the Р2Р lending mechanism in the system of funding small business entities within the agro-industrial complex. Nevertheless, most present-day small business entities within the agro-industrial complex have on staff, or engage on an outsourcing basis, specialists who are technically proficient in working with financial documentation in electronic form and effecting electronic payments, for most of the financials are now submitted to the tax agency and other government institutions in electronic form. Thus, even if the above negative factor does affect someone it will be just a minor portion of businesses within the Russian agro-industrial complex, but it will not seriously affect the development of alternative mechanisms for funding.

One of the key competitors of Р2Р lending is microfinance organizations. However, of late the latter’s reputation has been tarnished by a whole array of factors, from charging exorbitant interest rates on loans to wrongfully engaging a collection agency and lawsuits resulting because of this. This state of affairs in the market appears to only facilitate the development of Р2Р lending, under which there is virtually no risk of someone going to some shady collection agency, for lenders here are mainly natural persons, while small business entities within the agro-industrial complex mostly obtain their loans from several different lenders who are not related to each other. Also, as was noted earlier, the Р2Р lending mechanism, despite high levels of risk inherent to it, does not presuppose high interest rates for the use of borrowed funds. All this facilitates boosts in the amount of trust business entities put in Р2Р lending.

A negative factor that impedes the development of Р2Р lending in Russia and its active implementation within the framework of funding small business entities within the agro-industrial complex is the extremely low level of financial literacy among people, who not so much refuse to as simply do not know all the possible tools and mechanisms of the financial market they could use to invest their savings. This issue is even present in megalopolises, but it is a major concern in smaller cities. Unfortunately, it will be possible to mitigate the impact of said negative factor only in the long run and with support from the state – through courses for boosting the financial literacy of citizens conducted on a wide scale.

The successful implementation of Р2Р lending has been well facilitated by the development of Internet banking, with active Internet users, who are used to being provided with financial services in a fast, efficient, and timely manner, being expected to quite promptly comprehend and appreciate the Р2Р lending mechanism from the perspective of its “everyday use” convenience. Right now, most small business entities within the agro-industrial complex are headed by progressive executives who are keen to keep in step with the times and are perfectly knowledgeable about what is out there across the Internet space – so Р2Р lending platforms are not only unlikely to turn them off with their technical component (which, for the most part, is characterized by a simple, user-friendly interface) but may really interest them with the convenience of such services and the advanced functionality that enables you to keep track of all your transactions and deals in real time.

On the whole, despite some negative factors impeding the implementation of the Р2Р lending mechanism in the system of funding small business entities within Russia’s agro-industrial complex, there are really no insuperable barriers that would prevent smaller forms of business from taking advantage of Р2Р lending, an alternative way to obtain funding suggested by the authors.

Right now, projects associated with P2P lending are increasingly becoming the object of interest among larger players in the financial market, like commercial banks, collection agencies, and credit bureaus. This is facilitating the development of Р2Р lending in Russia as a whole and the agro-industrial complex in particular.

Despite the fact that there are wider, and in some sectors of the financial market increasingly wider, opportunities today for smaller forms of business within the agro-industrial complex to obtain funding, the issue of funding continues to be quite a major concern, and novel institutions, tools, and mechanism that could help resolve it may increasingly find support and firmly integrate into the financial system. The authors view Р2Р lending as one of the more effective mechanisms for funding small business entities within the Russian agro-industrial complex.

Just like any other market phenomenon, Р2Р lending is characterized by certain weaknesses, some of which were examined above, but these by no means diminish the actual merits of this mechanism for providing funding.

Going forward, demand for Р2Р lending among small business entities within the agro-industrial complex may increase not only due to a whole lot of advantages it offers but also in a climate of overall economic instability, mistrust of microfinance organizations, and declines in the number of banks in the market, as well as toughening requirements for their activity, which may promptly result in tougher recourse requirements to borrowers.

The issue of funding for smaller forms of business within the system of Russia’s agro-industrial complex continues to be a major concern, despite state support and the emergence in the market of new funding institutions, tools, and mechanisms which could help expand one’s roster of sources of funding. In this regard, the authors have been exploring the possibility of implementing an alternative mechanism in the system of funding smaller forms of business within Russia’s agro-industrial complex –P2P lending.

The research reported in this paper has produced the following findings.

It has been established that, in principle, P2P lending is no different from regular bank lending, but it has a number of distinctive characteristics of its own, which are as follows:

The authors have come up with a classification of possible auction-based Р2Р lending systems: an English auction, a Dutch auction, a closed auction for borrowers, a closed auction for lenders, and a joint-type closed auction.

The paper has identified some of the factors that facilitate and those that impede the implementation of P2P lending in the system of funding smaller business entities operating within Russia’s agro-industrial complex. The authors are inclined to believe that the negative factors should not seriously affect the implementation of Р2Р lending, while, going forward, its strengths should only attract increasingly more participants interested in using additional financial resources.

The authors are convinced their scientific hypothesis will be confirmed: P2P lending is going to help smaller forms of business within the Russian agro-industrial complex expand their potential for bringing in financial resources.

This research study was made possible by a grant from Plekhanov Russian University of Economics.

Civil Code of the Russian Federation: Part 2 No. 14-FZ of January 26, 1996. (in Russian).

Decree of the Ministry of Finance of the Russian Federation No. 66n ‘On Forms of Accounting in Organizations’ of July 2, 2010. (in Russian).

Federal Law of the Russian Federation No. 151-FZ ‘On Microfinance Activity and Microfinance Organizations’ of July 2, 2010. (in Russian).

Gaisin, R. S. (2015). Osobennosti formirovaniya tsen, sprosa, predlozheniya na agroprodovol'stvennom rynke Rossii [Characteristics of the formation of prices, demand, and supply in Russia’s agri-food market]. In Ya. S. Yadgarov, V. A. Sidorov, & V. V. Chapli (Eds.), Fenomen rynochnogo khozyaistva: Ot istokov do nashikh dnei: III Mezhdunarodnaya nauchno-prakticheskaya konferentsiya [The phenomenon of the market economy: From its origins to the present day: The 3rd international research-to-practice conference] (pp. 473–484). Krasnodar, Russia: Nauchno-Issledovatel'skii Institut Ekonomiki Yuzhnogo Federal'nogo Okruga. (in Russian).

Larionovа, I. V. (Ed.). (2017). Novoe prochtenie teorii kredita i bankov: Monografiya [A novel approach to the theory of lending and banking: A monograph]. Moscow, Russia: KnoRus. (in Russian).

Lavrushin, O. I. (2017). Novye yavleniya v razvitii kredita i institutsional'noi strukture bankovskogo sektora [New phenomena in the development of the lending system within the institutional structure of the banking sector]. Bankovskoe Delo, 2, 14–19. (in Russian).

Mach, T. L., Carter, C. M., & Slattery, C. R. (2014). Peer-to-peer lending to small businesses. Washington, DC: Federal Reserve Board.

Maksimova, T. P., & Bondarenko, N. E. (2017). Development of inter-firm cooperation in the Russian agro-industrial complex: Theory and practice. Espacios, 38 (33), 15.

Mirkin, Ya. M. (2016). Tsikly global'nykh finansov [Global finance cycles]. Problemy Teorii i Praktiki Upravleniya, 6, 51–56. (in Russian).

Patlasov, O. Yu., & Grakhov, A. A. (2016). Kraudfanding i set' P2P: Prognoz vzaimodeistviya i al'ternativnogo finansirovaniya v usloviyakh krizisa [Crowdfunding and the P2P network: A forecast for their interaction and alternative funding in a climate of recession]. Nauka o Cheloveke: Gumanitarnye Issledovaniya, 4, 204–218. (in Russian).

Slepov, V. A., & Chalova, A. Yu. (2017). Istochniki finansirovaniya ekonomicheskogo rosta v Rossii: Problemy i perspektivy [Sources of funding economic growth in Russia: Problems and prospects]. Nauchnyi Byulleten' Rossiiskogo Ekonomicheskogo Universiteta imeni G.V. Plekhanova, 1, 170–176. (in Russian).

Teteryatnikov, K. S. (2015). Platformy P2P kak instrument al'ternativnogo finansirovaniya: Mezhdunarodnyi i rossiiskii opyt [P2P Platforms as a tool for alternative funding: International and Russian best practices]. Menedzhment i Biznes-Administrirovanie, 2, 109–119. (in Russian).

Ustyuzhanina, E. V. (2016). The Eurasian Union and global value chains. European Politics and Society, 17, 35–45.

WebMoney Transfer. (2017). Retrieved from https://debt.wmtransfer.com/?lang=en&wmticket=

1. Plekhanov Russian University of Economics,Russia, 117997, Moscow

2. Plekhanov Russian University of Economics,Russia, 117997, Moscow

3. Plekhanov Russian University of Economics, Russia, 117997, Moscow. E-mail: olga.angel@bk.ru