![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (Number 13) Year 2018 • Page 28

Tatyana KHUDYAKOVA 1; Andrey SHMIDT 2

Received: 19/11/2017 • Approved: 16/12/2017

2. Analysis of last research and publications

ABSTRACT: In the era of globalization of the economy, causing increasing of uncertainty of the external environment of enterprises functioning, the need for methods of preventive management is dramatically increasing. These methods and approaches must improve the quality of management processes and the degree of forecasting of economic indicators and the stability of companies in the conditions of uncertainty. The article is devoted to the authors' methodological approach to the management of sustainability of enterprises based on the use of controlling technologies in the context of variable environment. Furthermore, the authors give the principles of interpretation of the level of financial and economic sustainability of the enterprise. The results obtained by the authors, can become a good tool to solve the problem of reducing the level of sustainability of enterprises in the conditions of considerable variability of the environment. That, in turn, is especially important during the global crisis. |

RESUMEN: En la era de la globalización de la economía, al aumentar la incertidumbre del entorno externo de funcionamiento de las empresas, la necesidad de métodos de gestión preventiva aumenta dramáticamente. Estos métodos y enfoques deben mejorar la calidad de los procesos de gestión y el grado de previsión de los indicadores económicos y la estabilidad de las empresas en condiciones de incertidumbre. El artículo está dedicado al enfoque metodológico de los autores para la gestión de la sostenibilidad de las empresas basado en el uso de tecnologías de control en el contexto de un entorno variable. Además, los autores dan los principios de interpretación del nivel de sostenibilidad financiera y económica de la empresa. Los resultados obtenidos por los autores, pueden ser una buena herramienta para resolver el problema de reducir el nivel de sostenibilidad de las empresas en las condiciones de considerable variabilidad del entorno. Eso, a su vez, es especialmente importante durante la crisis mundial. |

In spite of the fact that the first mention of controlling are dated back to the XV century and since the mid-twentieth century, this direction started developing quite intensely, at the present time there is no unambiguous interpretation of the category "controlling". However, almost all the researchers agree on a common opinion that this is a new concept of company management generating by the introduction of new technologies and management techniques.

The scientific approaches of Russian and foreign authors to the detection of the methods of the construction of the controlling system at the enterprise were analyzed within the work. This problematic was studied by Abelonyn, Lapaeva M.G., Nosaeva V.V., Hauzer M., Bekker V., Baltser B., Goncharova L., Khudyakova T. and Shmidt A. and others. However, in the reviewed literature the variability of the external environment is not taken into account but its calculation dramatically actualized in the period of global world crisis. At the same time it should be noted that in the reviewed literature, at first, the authors examine the various types of controlling, but do not talk about controlling stability minieconomic system. However, in our opinion, it is necessary to approach the construction of the system of the controlling from the position of the stability. At second, the works do not take into account the variability of external conditions, which undoubtedly influence on introduced system's efficiency.

Based on the analysis of the scientific literature the major preconditions of the occurrence, formation and further development of the conceptual category of "controlling" in foreign and Russian practices could be allocated. Among the basic prerequisites we would like to allocate, at first, the globalization of economic processes in society, the emergence of transnational corporations, the expansion of economic relations, including foreign trade, increasing of competition and scale of production etc, at second, the increasing of the variability of the environment of the enterprise's functioning, caused by the presence of the short and long economic waves, which are the reasons of crisis, at third, the information revolution, that provided the tremendous mobility of the information, the information capital and skilled personnel and which was caused by scientific and technological progress, at forth, changing of economic paradigms, that impacts on the transformation of the category "controlling".

All these prerequisites have a direct influence on the evolution of the conceptual category "controlling".

As we already noted the category "controlling" is much broader than "control". It implies a comprehensive, systematic management, which is based on the need to ensure a sustainable functioning and development of the minieconomic system in the long term via:

timely adaptation of the enterprise, correction of its strategic and tactical goals to the changes in the external environment, which are caused by variations in its parameters;

coordination of the activities, which are directed at the achievement of tactical objectives of the enterprise, with the strategic plan of the development of the minieconomic system;

analysis based on the developed criteria for the assessment of the current situation in the enterprise, in order to inform stakeholders and managers of different levels about the efficiency of the business entity;

adaptation of the organizational structure of the enterprise, directed at change of the management approaches, in order to increase the stability of the enterprise to the fluctuations of the external environment.

However, as already noted, the category of "controlling" is also not identical to the category "management". The majority of the modern authors divides their functions, noting the information and methodological functions of the controlling. Within the concept of the separation of the concepts of controlling and management there are different approaches to the definition of the first category. Controlling is interpreted as:

the tool for the methodological and information support of the process of the enterprise management;

the commenting function of the financial-economic activity of the enterprise;

the function of the informational support of the planning process in the enterprise.

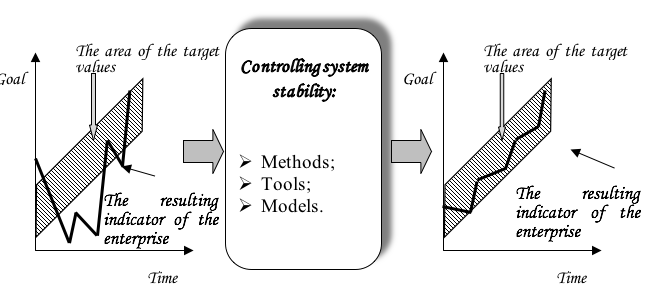

Graphically the essence of the implementation of the company controlling system of financial-economic stability can be represented in the form of the figure 1. There are fluctuations of the target indicator, which go beyond the boundaries of sustainable development of enterprises, at the entrance and at the output the target indicators enters the area of the stable values. We would like to point out that financial indicators, for example, the profit or the cash flow of the enterprise; the relative indicators, for example, profitability of sales or market share; and qualitative indicators, for example, quality of the products as well, could be the target indicator of the minieconomic system. Any of the given examples can be taken as the target indicator. It is necessary to remember that while assigning the goal in the form of a quality indicator it is needful to conduct its formalization.

Figure 1

The essence of the system of the controlling stability of the enterprises

Controlling of the sustainability implies a close cooperation of all the subsystems of the enterprise aimed at the establishment of adequate goals, taking into account not only the interests of the owners of the company, but also peculiarities of its functioning in conditions of variable environment.

This fact again proves the need for an integrated approach to the management of the minieconomic system on the basis of the using of the controlling as a tool of improving of financial-economic sustainability of the socio-economic system from the perspective of its dynamics.

The financial-economic sustainability will emerge from two kinds of sustainability: financial and economic. Moreover, these two indicators within our approach are not directly dependent on each other. We will consider it with the example. Let the coefficient of the autonomy be the resulting indicator for analyzing the financial activities and the net profit be the resulting indicator for analyzing the economic activities. It is possible that coefficient of the financial independence is lower than established level. In this case we could conclude that the enterprise is financial unstable. It could be economically stable even, for example, with a small amount of net profit or loss, if managers laid this size at the stage of goal-setting. Because in previous periods the situation at the enterprise could be worse, and realizing this fact, output to the profit zone could be interpreted as the economic sustainability. However, in general the company will not have sufficient level of financial-economic stability (Figure 2).

Figure 2

The interpretation of the level of the financial-economic stability of the

enterprises depending on the levels of the financial-economic stability

The type of the sustainability |

Economic instability of the system |

Economic stability of the system |

Financial instability of the system |

Financial-economic instability |

Financial instability / Economic stability |

Financial stability of the system |

Financial stability / Economic instability |

Financial-economic stability |

Thus, during the construction and implementation the controlling system in the enterprise it is necessary, at first, to consider two kinds of stability of an economic entity, at second, to select correctly the resulting indicators, which characterize financial-economic activity of the enterprise taking into account the principles that laid down at the stage of goal-setting. These requirements to the construction of the controlling system of the minieconomic system's stability will help the enterprise not only to apply proactive management of financial stability, to ensure a sufficient level of liquidity of the assets and to prevent the bankruptcy, but to determine the probability of achieving the goals by stakeholders in the process of managerial decision-making.

South Ural State University is grateful for financial support of the Ministry of Education and Science of the Russian Federation (grant No 26.9677.2017/ВР (Number for publication: 26.9677.2017/8.9)).

The work was supported by Act 211 Government of the Russian Federation, contract № 02.A03.21.0011.

Abelyan A.S. (2013). Building a system of structural dynamic stability of the enterprise in terms of modernization, Scientific review, vol. 6, pp. 178-183.

Becker B., Balttser B., Goncharov L. (2010). The interaction management and controlling: the experience of Germany and Russia, Controlling, vol. 36, pp 20-30.

Izotov A.V., Rostova O.V. (2017). Development of a system of sectoral investment priorities. Proceedings of the 29th International Business Information Management Association Conference - Education Excellence and Innovation Management through Vision 2020: From Regional Development Sustainability to Global Economic Growth, 2017, pp. 1812-1821.

Izotov, A.V., Rostova, O.V. (2017). The use of principal component analysis in the assessment of the investment climate regions. Economic, financial and management problems of the manufacture, (38), pp. 82-85.

Hauser M. (2014). Controlling – a purposeful planning and management of the company, URL: http://news.tut.by/economics/116110.html (reference date: 01.08.2017).

Khudyakova T.A., Shmidt A.V. (2017). Improving the efficiency of the enterprise's activity based on the implementation of the controlling system. Proceedings of the 12th International Conference on Strategic Management and its Support by Information Systems, pp. 46-52.

Lapaeva M.G., Nosaeva V.V. (2004). The factors and trends that determine the formation and development background of controlling an industrial plant, Bulletin, vol. 10, pp 99-103.

Shmidt A.V., Khudyakova T.A. (2015). Steady functioning of an enterprise in the conditions of variable economy, Mediterranean journal of social sciences, vol. 6/issue 4, pp. 274–279.

Zinovieva E.G., Usmanova, E.G. (2015). Enterprise stability factors, Scientific review, vol. 6, pp. 402-409.

1. South Ural State University, High School of Economics and Management, khudiakovata@susu.ru

2. South Ural State University, High School of Economics and Management, shmidtav@susu.ru