![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 38 (Nº 33) Año 2017. Pág. 37

Svetlana Valentinovna ROMANOVA 1; Tatyana Dmitrievna POPOVA 2; Irina Ivanovna SLATVITSKAYA 3; Daria Dmitrievna MIRONOVA 4

Received: 05/06/2017 • Approved: 25/06/2017

ABSTRACT: Regional development largely depends on the availability and quality of social infrastructure. Under conditions of instability of the competitive environment and various manifestations of the global crisis, contractors place a greater emphasis on the problems of cost reduction in the construction of social facilities. The deficiency of budgetary resources and the need to use private capital in the public interest explain the growing popularity of non-traditional government procurement systems in construction. One example is a public-private partnership (PPP). PPP projects are an area where the advanced methods for calculation of lifetime costs along with the method of target costs could be put into practice. One of the modern cost assessment methods, which can fill the gap in Russian business practices related to the management of accounting records, is the target costing. It assumes that the price of a product or service, in particular a service related to social infrastructure, does not depend on the cost of providing this service. In order to achieve commercial goals, the service provider should calculate the target cost based on the price and take actions to reduce the actual cost of construction to the target level with the efforts of management, engineers, designers, marketers, etc. The general objective of this study is to demonstrate the full applicability and usefulness of this cost control method, widely used in the practice of management accounting in developed countries. As a result of this study, it was concluded that the target costing method is applicable and is particularly useful in the construction of social infrastructure, and its results may provide support to decision-makers. |

RESUMEN: El desarrollo regional depende en gran medida de la disponibilidad y calidad de la infraestructura social. Bajo condiciones de inestabilidad del entorno competitivo y diversas manifestaciones de la crisis global, los contratistas ponen mayor énfasis en los problemas de reducción de costos en la construcción de instalaciones sociales. La deficiencia de los recursos presupuestarios y la necesidad de utilizar el capital privado en interés público explican la creciente popularidad de los sistemas no tradicionales de contratación pública en la construcción. Un ejemplo es una asociación público-privada (PPP). Los proyectos PPP son un área en la que se pueden poner en práctica los métodos avanzados de cálculo de los costes de por vida, junto con el método de costes objetivo. Uno de los modernos métodos de evaluación de costos, que pueden llenar la brecha en las prácticas comerciales rusas relacionadas con la gestión de registros contables, es el costo objetivo. Supone que el precio de un producto o servicio, en particular un servicio relacionado con la infraestructura social, no depende del costo de proporcionar este servicio. Para alcanzar objetivos comerciales, el proveedor de servicios debe calcular el costo objetivo basado en el precio y tomar medidas para reducir el costo real de la construcción al nivel objetivo con los esfuerzos de la dirección, ingenieros, diseñadores, comercializadores, etc. De este estudio es demostrar la plena aplicabilidad y utilidad de este método de control de costos, ampliamente utilizado en la práctica de la contabilidad de gestión en los países desarrollados. Como resultado de este estudio, se concluyó que el método de cálculo de costos objetivo es aplicable y es particularmente útil en la construcción de infraestructura social, y sus resultados pueden proporcionar apoyo a los responsables de la toma de decisiones. |

The construction of infrastructure facilities is one of the most important areas of responsibility of the municipal services, which directly affects the quality of life of the population. Modern urban development projects involve the construction of social, commercial, engineering and transport infrastructure, the state and the quality of which has a significant impact on the comfort of the residents and also not least affects the cost of housing in a certain neighborhood.

Since the economic development of regions and the country as a whole largely depends on the availability and quality of social infrastructure and related services, this area needs to become more effective. Social infrastructure projects are rarely profitable in themselves for commercial purposes (Sobotka, & Czarnigowska, n.d.).

Unstable and competitive economic environment requires that the main factors, such as functionality, price and development time of products and services, be managed properly. This is necessary in order to ensure that the providing organization is commercially successful in the long run (Mărginean, & Țepeș, 2014).

Modern information systems and technologies are a means for the formation of the material and technical base for the development and reproduction of human capital, the increase of labor productivity and efficiency of economic activity, thus creating conditions for the growth of social significance (Cherkesova et al., 2016).

The success of implementing urban infrastructure projects is considered in terms of the efficient use of the limited budget resources to provide social and communal services as soon as possible and in the most cost-effective manner. As for costs for the operation and maintenance of the facility, infrastructure projects usually involve thorough preparation and significant capital costs. Over the years of operation, the infrastructure accumulates significant amounts of maintenance costs, the level of which is closely related to the project designs and decisions made at the initial stages of construction.

Any viable tool, the use of which allows controlling and reducing costs, becomes a real challenge for government authorities and companies engaged in infrastructure construction. In order to win tenders, construction companies need to have a competitive advantage that can be achieved due to the highest cost-effectiveness indicators for construction and competent cost management.

Production costs must be planned and managed in accordance with the construction estimates, the cost of which is borne by the customer; moreover, they are normally decreased (lower cost means higher profit) without compromising the quality. In many cases, this involves close collaboration between suppliers, developers, contractors and self-regulatory organizations to find better organizational and design solutions to the mutual benefit of all participants of the construction process.

One of the management approaches used in a highly competitive construction industry is the target cost calculation (target costing). Target costing is one of the modern methods of cost management and, unlike other calculation methods, it allows monitoring and timely adjusting the project, starting with the design phase, adapting the costs to the target unit price of construction works. "Target costing" refers to a number of methods used in traditional cost management, such as contract and cost management, along with the target cost (Zimina et al., 2012). The introduction of target costing will help avoid budget overruns in the implementation of the construction of urban infrastructure projects.

The basic characteristics of strategic management should ultimately be aimed at preserving, dynamically developing and effectively managing the company's property. For these purposes, adequate information and analytical support is needed. In general, the accounting and analytical system is a set of accounting information and the analytical data obtained on its basis, intended for decision-making (Krokhicheva, & Romanova, 2013).

The importance of strategic analysis and its ability to manage costs in the implementation of infrastructure projects predetermine the need to create a methodology for targeting costing.

The objective of this study is to explore the applicability of a modern cost management system in the process of developing public infrastructure projects.

The theoretical basis for the study is the literature on economics and finance. In order to reflect the strengths and weaknesses of the target costing method in the implementation of urban infrastructure projects, the authors of this study reviewed the publications of domestic and foreign authors on cost management and, in particular, on the application of the target costing method.

The study uses statistical data reflecting the volume of the construction of social infrastructure in the Central Federal District, the actual data on management accounting of construction companies.

In order to achieve the desired objective, several challenges have been solved:

The problem of the construction of social infrastructure has become particularly relevant with the development of mass housing construction. If in case of infill construction projects in the most populated areas, the need for social services could be solved by the existing institutions, in complex development of the territory this is impossible both because of the limited capacity of existing facilities and because of their location outside the regulated radius of accessibility (Surveyor International Group, 2014).

The Central Federal District of the Russian Federation significantly lags behind the rest of Russia on the development of social infrastructure (with the exception of the Crimean Federal District). The comparative indicators for the commissioning of social infrastructure facilities in the federal districts of the Russian Federation are presented in Table 1.

Table 1. Indicators for the commissioning of social infrastructure

facilities in the regions of the Russian Federation in 2015

Regions of the Russian Federation |

Commissioning of general education institutions' capacities, student places per 10,000 population |

Commissioning of preschool educational organizations' capacity |

Commissioning of hospital organizations' capacities , beds per 10,000 population |

Commissioning of outpatient and polyclinic organizations' capacities, visits per shift |

Russia |

4.533 |

9.796 |

0.292 |

1.621 |

Central Federal District |

4.585 |

8.410 |

0.241 |

1.733 |

Northwestern Federal District |

4.520 |

7.956 |

0.488 |

1.803 |

Southern Federal District |

0.711 |

8.898 |

0.034 |

0.451 |

North Caucasian Federal District |

24.566 |

7.169 |

0.667 |

1.160 |

Volga Federal District |

1.902 |

9.524 |

0.187 |

2.196 |

Ural Federal District |

3.023 |

16.745 |

0.182 |

1.707 |

Siberian Federal District |

2.512 |

12.497 |

0.164 |

1.341 |

Far Eastern Federal District |

5.236 |

10.652 |

1.369 |

2.413 |

Crimean Federal District |

0.000 |

2.266 |

0.087 |

0.000 |

Reducing this backlog will require significant investments from the federal and regional budgets in the coming years and will lead to serious changes in the regional structure of the volumes of social facilities commissioning.

In three years, the volume of construction works in the Central Federal District has decreased by 29.3%, while in the country as a whole in 2015, the dynamics of executed construction volumes was positive (+2.1%).

The decrease in construction volumes took place in all the District's subjects, with the exception of the Rostov Region, the Republic of Adygea and the Volgograd Region. Most significantly – by 48.8% - the volume of construction works decreased in the Krasnodar Region, by 37.5% – in the Astrakhan Region, and by 34.1% - in the Republic of Kalmykia (see Table 2).

Table 2. Volumes of construction works in the subjects

of the Southern Federal District in 2015, mln. rubles

Subjects of the Southern Federal District |

2013 |

2014 |

2015 |

Alternation |

|

+/- |

% |

||||

Southern Federal District |

731,522.8 |

582,210.3 |

517,692.6 |

-213,830.2 |

-29.2% |

The Republic of Adygea |

9,651.6 |

10,280.1 |

11,545.8 |

1,894.2 |

19.6% |

The Republic of Kalmykia |

3,862.8 |

8,124.0 |

2,545.0 |

-1,317.8 |

-34.1% |

The Krasnodar Region |

480,663.6 |

316,186.5 |

246,143.4 |

-234,520.2 |

-48.8% |

The Astrakhan Region |

52,284.9 |

42,049.3 |

32,698.3 |

-19,586.6 |

-37.5% |

The Volgograd Region |

58,597.4 |

62,336.1 |

69,578.0 |

10,980.6 |

18.7% |

The Rostov Region |

126,462.5 |

143,234.3 |

155,182.1 |

28,719.6 |

22.7% |

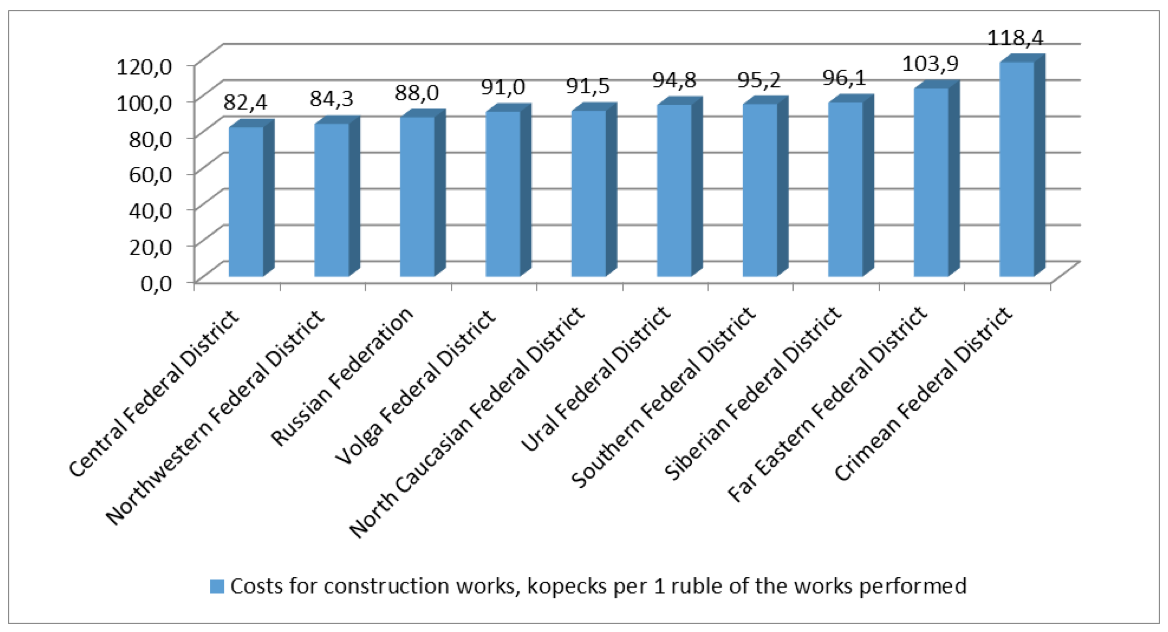

Despite the decrease in the level of construction costs in the Southern Federal District, by the end of 2015, this indicator significantly exceeds the average Russian value (see Figure 1).

Figure 1. Costs for construction works of the subjects of the Russian

Federation by the end of 2015, kopecks per 1 ruble of the works performed

In the coming years, the federal government plans to significantly change the current situation by increasing the rate of social facilities commissioning in the most problematic regions in this respect. First and foremost, this should be facilitated by the implementation of the federal target program "South of Russia for 2014-2020 years".

At present, there is an established pattern when the requirements for the construction of social infrastructure are mandatory conditions for the implementation of complex development projects. At the same time, the construction costs are borne by the developer. Otherwise, for whatever reasons, its project will not be approved by the local authorities.

On the other hand, the construction of social infrastructure facilities is not profitable for developers from the economic point of view. The payback period of such facilities is either very long or nonexistent.

The implementation of such a policy leads to the fact that the costs for the construction of social facilities ultimately passed on to consumers – home buyers. Despite the fact that the payment for the construction of social infrastructure costs should be carried out of the developer's profit, the developer nevertheless indirectly includes these costs in the price per square meter of commissioned living space.

However, it should be noted that this practice reduces the availability of housing and social facilities for the population in need of better housing conditions. As a result, the problems of low housing provision and a high proportion of the population living in dilapidated and emergency housing remain unresolved in the subjects of the Southern Federal District.

One of the factors determining the final result of the project in terms of its economic impact on the project participants, buyers and the public is the system of public procurement in the construction sector. The procurement system can be defined as a method of allocating responsibility for the planning, design and construction of the constructed facility for the project participants.

In the public sector, where the task of the authorities is to implement projects that are crucial for the development of the community, the key factors are effective management of public budget funds, accountability and transparency of decisions.

Technological progress and the consequent complexity of the projects explain the growing popularity of new procurement systems aimed at improving the efficiency of public projects. This can be done through:

- recruitment of external specialists to assist at the stages of creation and planning, as well as coordinating the work of designers and developers;

- entrusting the design and construction to one contractor (design and construction, design and management). Design and construction stages may overlap. The parallel development process allows the designer to make changes to the project without interrupting other processes. It is possible to impose strict financial discipline on the contractor to ensure the completion of the project in accordance with the budget.

Assignment of additional tasks to the contractor: to plan the project, choose the sources of financing and fund the project until it begins to operate (contracts, the owner is the party that pays for commissioning and maintenance of the facility). The contractor is thus related to the costs during the entire project.

The introduction of economic incentives for the project participants to improve the long-term effect of the project in the form of PPP. The public owner provides a concession to the enterprise that plans, finances, designs, constructs and operates the facility and restores its expenses from the proceeds of sale of services at the facility.

Regardless of the procurement method, it is necessary to evaluate the project costs to set a budget and manage costs in order to achieve the best price-quality ratio. Especially if the constructed object includes not only high initial costs but also significant costs in its future operation (maintenance, renovation, heating, modernization, etc.).

Cost management in the implementation of public infrastructure projects can be defined as a system of techniques and methods for planning, implementing, measuring and reporting in order to increase the productivity of services, their management and related processes through cost optimization. Cost management is a long-term process aimed at the elimination of all kinds of activities (and their cost) that do not add value to the final product or services offered to consumers. The consumer itself is multidimensional. Each of them pursues their own interests and goals, though two basic parameters – the quality and price of the product – are equally important to all customers (Slatvitskaya et al., 2016).

In the case of organizations dealing with construction, such as designers, contractors or project managers, there are three objectives for cost management (Potts, 2008):

The third objective is the need for an accurate assessment of the total cost of the project and, in particular, the cost of construction in the early stages of the project, when the project does not exist yet. This early assessment is the basis for the feasibility study of the project owner which will help him make a decision on whether the project should be approved or not.

The target costing method could become one of the methods used in cost management in the construction of infrastructure projects.

As for the method of target costing, it is widely considered in the economic and financial literature. The work of Feil, P., Yook, K. and Kim, I.W. notes that the target costing (TC) has appeared in the manufacturing industry in the early 1930s (Feil et al., 2004) and has proved to be a powerful strategic tool for profit management and planning. According to the authors Briciu S., Sorinel C., Rof L.M. and Topor, D. (2010), the target costing method was developed in Japan in the automotive industry in the 1980s and is based on the idea that the selling price of a product is determined by the market.

The application of the target costing method in Russian companies was considered in the works of Kurilov K.Y., Kurilova A.A., Redchenko K., Novikova I.V., Sheshukova T.G. and others. At the same time, in the scientific literature one can find only scanty reports on theoretical and practical questions of the application of target costing (Pennanen et al., 2010).

The main costing principle is that the calculation of allowable (normative) costs is carried out by marketing research and forecasting the target price that the buyer is willing to pay for the products with specific characteristics.

The similarity in the processes of development and production of construction projects makes it possible to calculate costs the for the construction of public infrastructure projects. According to data cited in the work of Jacomit, A.M., in Japan, about 15% of construction companies calculate target cost on the base of production data (Jacomit et al., 2008).

The study and systematization of approaches, reflected in the specialized literature, allows identifying several logically consistent and interrelated stages in the application of the target costing method:

Step 1. Target pricing based on the analysis of a competitive market environment.

In this respect, the method is different from other costing tools. This method is based on the market analysis and product sales and allows putting a price bringing fixed profit to the company. At this stage, it is necessary to define needs and expectations of the population in relation to social services facilities and the price they are willing to pay for them.

The target price can be established on the constructed object – this is the amount that the public owner is willing to pay for it, as a result of its budget, its economic analysis and the urgency of the project. This amount is the basis for calculating the contractor's target value.

Step 2. Setting the target margin (profit).

Target profit is the ultimate interest of the company, "the real reason" of its involvement in the business. Target cost consists of distributable cost elements. In the specialized literature on account management, there are several costs. The cost, which can be attributed to expenses, may consist of variable production costs (raw materials, piecework wages), unit costs (depreciation, preparatory works, equipping with measuring and monitoring devices and tools), other expenses (general production and administrative costs), and investment costs.

Step 3. Valuation of the estimated and target cost. This is a high-technology and special-purpose stage where a special role is given to engineers and technicians who help to access the estimated costs. Then the difference between the estimated and target cost is determined.

Target costs expected by the contractor to guarantee the income received at the stage of signing the contract can be characterized by the formula:

TC = R – M (1)

TC – target cost of the project distributed throughout its life cycle,

R – revenues from the sales of services,

M – profit amount required by the contractor (the desired level of return on capital)

Step 4. Calculation of the estimated cost of production and evaluation activities. At this stage, the total costs are calculated by summing the direct and indirect costs attributed to production included in the "target costing" analysis.

Step 5. Calculation of the amount to be reduced/adjusted on the costs basis. At this stage, it is possible to adjust the cost of the difference between the estimated and the target cost. If this difference is positive, a review of the estimated cost is required to match the target cost. If the difference is negative, it means that the target value exceeds the estimated value and the situation is favorable for the company.

It is expected that the greatest benefits from the application of target costing in the construction of social projects are associated with the PPP.

The product sold by the contractor (private partner) and the source of its income is not a building, but the infrastructure service, which actually is a mass product, which must be supplied for a long period of time. The contractor is responsible for all phases of the project implementation and is interested in the rational allocation of costs throughout the life of the project.

The target price of a product (that is, services based on an infrastructure) is regulated by the price elasticity of demand (if the services are purchased directly by users) and the elements of the public regulator (setting the maximum price and the minimum level of capacity), in case the infrastructure facility is crucial for public policy purposes. If the service cannot be paid directly by users, the public authority cannot pay the contractor through budgetary funds, in that case the price could be determined by economic analysis of the public buyer.

The results of the study lead to the following conclusions:

In conclusion, it should be noted that the first step in applying the target costing method in social infrastructure construction projects is rather complicated. The contradiction of the market price associated with the public service inevitably depends on the public policy and cannot often be unambiguously set by the market research methods and thus should be discussed with the public authority. The expenditure amount included in the analysis of target costs will also be far greater in the case of public infrastructure projects compared to the manufacturing practices. This is due to the fact that additional costs are directly related to the project and its final product (public social service).

Briciu, S., Sorinel, C., Rof, L.M., & Topor, D. (2010). Contabilitatea si control ul de gestiune [The Accounting and the Management Control] (pp. 386-387). Alba-Iulia: Aeternitas Publishing House.

Cherkesova, E.Y., Breusova, E.A., Savchishkina, E.P., & Demidova, N.E. (2016). Competitiveness of the Human Capital as Strategic Resource of Innovational Economy. Journal of Advanced Research in Law and Economic, VII(7(21)), 1662-1667.

Feil, P., Yook, K.H., & Kim, I.W. (2004). Japanese Target Costing: A Historical Perspective. International Journal of Strategic Cost Management, Spring 2004, 10-19.

Jacomit, A.M., Granja, A.D., & Picchi, F.A. (2008). Target Costing Research Analysis: Reflections for Construction Industry Implementation. In 16th Annual Conference of the International Group for Lean Construction, Manchester, UK, 16-18 July 2008.

Krokhicheva, G.E., & Romanova, S.V. (2013). The System of Information-Analytical Support of Strategic Management. Components of Scientific and Technological Progress, 16, 68-71.

Mărginean, R., & Bobescu, A.T. (2014). The Cost Control by Applying the Target Costing Method in the Construction Industry. Sea – Practical Application of Science, II-1(3), 348-357.

Pennanen, A., Ballard, G., & Haahtela, Y. (2010). Designing to Targets in a Target Costing Process. In 18th Annual Conference of the International Group for Lean Construction, Haifa, Israel, 14-16 July 2010.

Potts, K. (2008). Construction Cost Management Learning from Case Studies. Taylor & Francis e-Library.

Slatvitskaya, I.I., Mironova, D.D., Zibrova, N.M., Romanova, S.V., & Ryabocon N.A. (2016). Import substitution in agrarian sector as the basis of technological breakthrough to innovational production. International Journal of Economics and Financial Issues, 6(2), 253-259.

Sobotka, A., & Czarnigowska, A. (n.d.). Target Costing in Public Construction Projects. Retrieved May 3, 2017, from https://www.researchgate.net/publication/265924943.

Surveyor International Group. (2014). Mekhanizmy obespecheniya sotsialnoi infrastrukturoi proektov zhilishchnogo stroitelstva [Mechanisms for Providing Housing Projects with the Social Infrastructure]. St. Petersburg. Retrieved May 3, 2017, from http://sig-company.ru/files/pdf/predlozheniya_po_obespecheniyu_spb_ob_ektami_soc_infrastruktury_1.pdf.

Zimina, D., Ballard, G., & Pasquire, C. (2012). Target Value Design: Using Collaboration and a Lean Approach to Reduce Construction Cost. Construction Management and Economics, 30, 383-398.

1. The Institute of Service and Business (branch) Don State Technical University, 346500, Russia, Shakhty, Shevchenko Street, 147

2. The Institute of Service and Business (branch) Don State Technical University, 346500, Russia, Shakhty, Shevchenko Street, 147

3. The Institute of Service and Business (branch) Don State Technical University, 346500, Russia, Shakhty, Shevchenko Street, 147

4. The Institute of Service and Business (branch) Don State Technical University, 346500, Russia, Shakhty, Shevchenko Street, 147