![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 38 (Nº 09) Año 2017. Pág. 28

Marcos Malinverni PAGLIOSA 1; Sidnei GRIPA 2; Wallace Nóbrega LOPO 3

Recibido:09/09/16 • Aprobado:12/10/2016

ABSTRACT: The world of business is dynamic and full of changes that occur with increasing frequency. In the constant quest for survival, companies need to offer attractive products to their customers who are each day more demanding. Productivity and competitiveness are part of the ordinary routine of a company. However, to be in fact productive and competitive, every company must first master quality management and know how much it costs. In this sense, quality management costs becomes a very important and strategic tool with the potential to contribute to any organization, regardless of the size or business field, helping to positioned it always ahead of the competition. The aim of this study was to identify and measure the quality costs in the manufacturing process of a starter drive gear produced in a medium-sized company that operates in the metal mechanical sector and that supplies auto parts to the world's leading car manufacturers. To achieve this purpose, a literature research was carried out, predominantly in a qualitative exploratory manner, and also a case study, where the quality appraisal costs of deferent components were identified and measured over the stages of the manufacturing process. |

RESUMO: O mundo dos negócios é dinâmico e cheio de mudanças que ocorrem com frequência crescente. Na busca constante pela sobrevivência, as empresas precisam oferecer produtos atrativos a seus clientes que estão cada dia mais exigente. Produtividade e competitividade são parte da rotina normal de uma empresa. No entanto, para ser de fato produtivas e competitivas, cada empresa deve primeiro gestão qualidade mestre e sei quanto custa. Neste sentido, os custos de gerenciamento de qualidade torna-se uma ferramenta muito importante e estratégica com o potencial de contribuir para qualquer organização, independentemente do tamanho ou área de negócios, ajudando a posicionou sempre à frente da concorrência. O objetivo deste estudo foi identificar e medir os custos da qualidade no processo de fabricação de uma engrenagem de acionador de partida produzida em uma empresa de médio porte que atua no setor metal mecânico e que fontes de auto peças para fabricantes de carro principais do mundo. Para atingir este objectivo, uma pesquisa da literatura foi realizada, predominantemente na forma qualitativa exploratória e também um estudo de caso, onde os custos de avaliação de qualidade de componentes deferentes foram identificados e medidos sobre as fases do processo de fabricação. |

Within the rapid pace of change in the quest for survival, organizations need to offer the best product to their customers and that means working with high quality standards. In this context, the quality becomes a key, because only through productivity it is achieved, generating competitiveness, which also ensures the ultimate goal of all organizations: their survival.

The market has become global and the relationship between quality and competitiveness is one of the most important issues of economy. Aware of the fundamental importance of quality and its management, this study analyzes and presents the numerous benefits of having an efficient quality management on an organization through the knowledge and control of quality costs. According to Robles Jr. (1994), management and measurement of quality costs are becoming a powerful differential, a strategic issue of fundamental importance, because it is a tool that has the potential to improve quality as well as to enhance the administration of the entire company. In Brazil, the implementation of quality management costs was anticipated, taking the lead of the organizational change process in a way never seen before in the economic history of the country.

This study deals with quality issues, quality costs and concentrates in the quality appraisal costs, bringing a case study where the theory was put into practice and applied on the company throughout the manufacturing stages of a starter drive gear produced in a medium-sized company with approximately 1,000 employees and 55 years of existence. The company operates in the metal mechanical sector as a supplier of auto parts to the world's leading car manufacturers exporting its products to over one hundred countries for the independent aftermarkets (IAM) and the original equipment manufacturers (OEM).

Why is the quality becoming increasingly important? The answer for this question can be answered in different ways. One is simply because there are thousands of products and suppliers that are increasing each day in the entire world, which means that in order to compete, companies need to sell a product or service of good quality. Otherwise, they will not be able to get market shares and without these, companies do not survive!

The relationship between quality and competitiveness is one of the most important issues in the current economy. According to Juran (1998), when a company can increase the quality of their product it also increases their productivity which consequently increases their competitiveness. In other words, the ability of your product or service to stand out among other competing products increases, whether by issues of cost, price or characteristics of the product or service. In this sense, the subject of quality costs is justified by itself, and becomes an important tool for any company to stand out against the others.

Several authors of national and international renown have studied the subject of quality costs due to its importance. Some key concepts are presented below:

Quality costs refer to all expenses incurred by the company, either inside or outside the same, for the care and maintenance of a satisfactory economical level of quality and reliability of the product, Rontodaro (1996). According to Berliner and Brimson (1992), Horngren et all (2000) and Baiman, Fischer and Rajan (2000), quality costs are costs incurred by a company to prevent quality problems, assessing the quality and controlling the product’s internal or external failures.

Still Feigenbaum (1994), defines the quality costs as the costs associated with the definition, creation and quality control, as well as evaluation and feedback of the correspondence with the performance requirements, reliability, and security; and finally, the costs associated with the consequences from failures in response to these requirements, both within the company and in the hands of customers. According to Mattos (1997), quality costs can be defined as any manufacturing or service costs exceeding those that would have occurred if the product or service would have been manufactured or provided perfectly right the first time.

Quality costs are factors that the organization must control with regard to prevent flaws in the process, because, as Garrison and Noreen (2001) say, the quality costs refer, in the contrary, to all the expenses to be made in order to prevent defects, or those made to attend the defects that already appeared.

In a more practical way, we can say that quality costs are all costs that the company has to endure to guarantee the production of their product and maintain later a satisfactory level of quality that meets the expectations of its customers. These costs are basically divided into non-avoidable costs and avoidable costs, including the internal and external environment of the company. That is, the quality problems that occur inside and outside the company.

According to Juran (1998) in many companies the quality costs oscillates between 20 and 40% of sales, being the majority avoidable costs. That is, they are costs originated by low quality and most of them are not perceived or properly identified by the company’s administration. In this sense a quality management costs system that can identify and analyze this information becomes an important tool for the products quality management as well as for the entire organization.

Over time techniques and methods were being improved so that the quality management costs could establish a common and simple language for measurement and evaluation of information, thus facilitating its application and understanding, and consequently opening the possibility to demonstrate that quality provides profit and productivity increments for the company, improving the customer's acceptance and satisfaction towards their products and services. Mattos (1997).

Formerly the concept of quality costs only addressed the total avoidable quality cost. With the passage of time, the concept evolved to encompass all costs required to obtain the required quality and cost of internal and external faults. Subsequently, the quality cost surpassed manufacturing, and was also applied to all areas of the company. Field (2003). Quality costs can be better explored, and should be equal in importance to other categories of costs, such as labor costs, engineering costs and sales costs (Feigenbaum, 1994).

Companies that seek to be competitive, to remain active in the market, need to own a smart strategy that may offer an advantage to locate them ahead of the others. Therefore, for this strategy to be effective and guide the company in the desired direction, it is essential to access and control key information about the company. Following this line of reasoning, quality management costs constitutes an important tool for the efficient management of quality; through the quantification and analysis of cost categories it guides the administrations’ decision-making process, becoming a strong ally to the company's strategy.

According to Robles Jr. (1994) the quality management costs are more than just the measurement of expenses caused by low quality, since it can also be used as a tool to assist in the integration of the control of quality cost to obtain important information for making strategic decisions. The correct understanding of the role-played by the quality management costs allows the company to answer a series of relevant questions that were previously not answered with proper certainty.

Said author also highlights several important objectives and issues attended by quality management costs, among which are the following:

a) Measure the quality programs through physical and monetary quantifications;

b) Identify in reality how much the company is wasting by a lack of quality;

c) Determine the distribution of costs among the various categories of quality costs;

d) Define and prioritize objectives for quality programs with the intention of obtaining faster and better results for the company;

e) Restate the quality as the main strategic objective for the company when necessary;

f) Set objectives and resources for the staff training;

g) Increase productivity through quality;

h) Disclose the financial impact of decisions that involve quality improvement, presented in quality costs reports;

i) Facilitate the elaboration of a quality costs budget, allowing the use of resources;

j) Identify in reality how much the company has invested in the different categories of quality costs.

Feigenbaum (1994) separates quality costs into two broad categories: control costs and controlled failure costs. These two categories are further subdivided as follows: control costs include the prevention and appraisal costs. It already controls failures including the costs of internal failure and external failure.

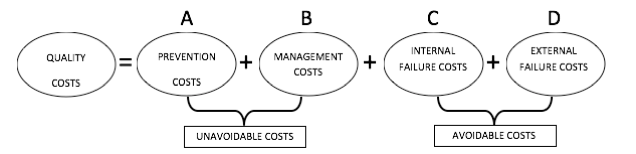

Juran (1998) divides the quality costs in two main areas when it says that the costs to obtain a certain level of quality can be divided into avoidable costs and unavoidable costs. The unavoidable costs are associated with the prevention and appraisal. Avoidable costs are associated with defects and faults of the products identified within the company and outside the company, when the product is already on the market, as shown in Figure 1:

Figure 1 – Categorization of quality costs

Source: Juran, (1998)

Also, according to Juran (1998) and Horngren et all (2000), avoidable costs (internal failure costs and external failure costs) are a real gold mine, as these costs could be greatly reduced by improvements in the quality system which would generate a reduction in costs.

According to Robles Jr. (1994) The quality costs are grouped into categories that relate to each other. The application of resources in a particular category entails variations in the amount of costs in another category. The more you invest in prevention and control, the smaller the chances of occurrence of internal and external flaws in the process.

Although there are various sources in the literature, there is some agreement in separating quality costs into four categories, as shown in Figure 2:

Figure 2 – Categorization of quality costs

CATEGORIZATION OF QUALITY COSTS |

A - PREVENTION |

These are costs associated with project activities, implementation and operation of the quality appraisal system, including the appraisal and audit system in the entire production cycle (from the production moment to after-sales). It refers to expenses incurred for the purpose of avoiding defects. |

|

B - APPRAISAL |

|

These are costs associated with the measurement, evaluation and auditing features of raw materials, components and products to ensure conformity with quality standards. It refers to the inspection of the proper quality appraisal costs system. |

|

C – INTERNAL FAILURES |

|

Costs associated with materials, components and products that do not meet quality standards, causing production losses, and that are identified when the product is still in the company. That is, failure costs identified inside the company. |

|

D – EXTERNAL FAILURES |

|

Costs generated by the distribution of non-compliant or defective products to customers / consumers. That is, failure costs identified outside the company. |

Source: Robles Jr. (1994)

According to Toledo (2002), the appraisal costs are associated with the measurement, appraisal and auditing features of raw materials, components and products to ensure conformity with quality standards. It refers to the inspection activities costs (quality appraisal) itself.

Appraisal costs are those costs incurred with inspections, tests and audits required to determine and ensure compliance with the requirements during all stages of the execution of a product or a service, highlighting among these the appraisal cost related to inspections and testing of the performance of services or products and the appraisal costs that results from the review of data inspection before elaboration of the product or termination of services.

Shank (1997), presents an example of a company that decided to double its investments in prevention and appraisal activities and could further reduce their costs of internal and external failures in more than 80%. Based on his research, the author also comments that for every dollar invested in prevention activities the company generated savings up to ten dollars on the failures costs appraisal.

Regarding the appraisal cost, which is the focus of this work, the result follows the same logic, that is, a greater investment in appraisal costs will generate naturally higher costs with internal faults, resulting in a more effective and robust administration within the company covering a greater amount of items. In contrast, the costs of external failures that are the villain of quality costs will decrease considerably.

Further, for a better understanding, the elements, definition and associated costs of the appraisal costs, focus of this study, are shown separately in Figure 3:

Figure 3 – Categorization of appraisal quality costs

B - APPRAISAL |

COST ELEMENT |

CONCEPT |

ASSOCIATED COSTS |

1 – Inspections and audits in acquired products and services. |

These are costs of inspections and/or audits of the acquired products and services, needed to determine their suitability. Such activities can be performed as part of the incoming inspection or as an inspection performed by the own provider. |

- Testing and acceptance testing of the supplier and control programs; - Testing and acceptance testing at a laboratory; - Trials and tests and receiving; - Qualification or the supplier’s approval of products or services. |

|

2 – Appraisal of the operations (manufacturing or services) |

These are costs incurred with inspections, tests and audits required to determine and ensure compliance with the requirements at all stages of execution of a product or a service. |

- Analysis of information for execution; - Inspection and tests of prototypes; - Product Approval or processes by official agencies; - Inspections and tests during the performance of services or products; - Laboratory tests; - Review of inspection data before shipment of goods or completion of services; - Staff involvement with the appraisal of quality; - Acquisition and depreciation of inspection equipment; -Maintenance, adjustment, calibration of the inspection equipment; - Materials consumed during inspections and testing; - Audits of the quality of the product or service. |

|

3 – External appraisal |

These are the costs related to the appraisal carried out at the customer properties, before the official acceptance of the product. |

- Transport Inspection and storage time; - Inspection and testing during assembly on the client; - Pre-operational tests. |

Source: Shank (1997)

The approach to the problem was achieved through a qualitative research, as the measurement of some results was not possible. Since the research is about the quality costs, a subject considered as new in the "market", the objectives were covered by an exploratory research, involving also literature review, analysis of examples and contact with people who have had practical experience. Gil (2007) states this kind of research is intended to increase familiarity with the problem in order to make it more explicit, and has as main objective the improvement of ideas or the discovery of intuitions.

The literature was also used aiming to examine content for the reasoning and learning. According to Saunders, Lewis and Thornhill (2012), the literature is sustained in existing base materials, such as books and scientific articles. Regarding the technical procedures, it is a case study because the data collection was performed in bibliographic form. The topics covered in the data collection were: accounting information system, quality costs and quality appraisal costs.

The case study was carried out in a national midsize business with approximately 1,000 employees and 55 years of existence. The company operates in the metal mechanical sector as a supplier of auto parts to the world's leading car manufacturers exporting its products to over one hundred countries in the aftermarkets (IAM) and original equipment manufacturers (OEM).

Through documentary study, reports and charts it was possible to examine the productive processes and quality systematics. Another form of data collection was the use of observation as participant, thus collecting the maximum possible information, correlating them with the theory versus practice.

In this chapter, we sought to identify and understand the current situation of the company, on the concepts related to quality costs, more specifically on the quality appraisal costs that are present in the manufacture of products.

Through exploratory research and survey data collection with the sectors of production, process engineering, quality and cost, it can be seen that the company does not measure, and therefore does not know how to control the existing appraisal costs in the production of their products. Starting from the fact that the company does not measure and therefore does not control the appraisal cost of its manufacturing processes, the objective of this work was determined to be the study of such appraisal costs in the production of their products.

As the company has a huge amount and variety of products, it was defined in agreement with the administration of the quality sector that the best way to understand, identify, and measure a product appraisal costs would be to choose a specific product and use it as a "test model", by applying this test the theoretical concepts regarding the appraisal costs. Thus, the chosen product for “test model” was the starter drive gear code 1000.

Why the starter drive 1000 was chosen? The starter drive 1000 is a starter which has a design and standard process like the vast majority of the remaining produced starters, meaning that when they are identified, the appraisal costs of the starter drive 1000 was similar, comprising an approximate idea of the appraisal cost of many other starters that have the same manufacturing process.

Another positive point is the fact that the starter is an item sold to the Ford, an original equipment manufacturer (OEMs) and so it is produced in accordance to the most strict quality requirements of the automotive industry. The starter 1000 also has a high-volume production, above average. Due to this favorable combination of factors, the decision was taken to use it in the test model.

All starters produced in the company have a list of components that are designed and controlled by the product-engineering sector. In this list are registered and differentiated the codes and the names of all components, as well as the required amount of each one, so that the starter drive can be produced and assembled correctly and according to the original design. Below there is the list of the components of the starter drive 1000, as shown in Fig. 4:

Figure 4 – List of the components of the starter drive gear 1000

Starter Nº 1000 |

|||

List of Components |

|||

Nº |

Part code |

Part name |

Quant. |

1 |

007 01760 |

Ring Bearing |

1 |

2 |

007 01992 |

Pressure Ring |

1 |

3 |

013 00840 |

Washer |

1 |

4 |

013 01040 |

Washer |

1 |

5 |

135 00150 |

Crown |

1 |

6 |

220 00740 |

Shaft |

1 |

7 |

226 00890 |

Wearing Ring |

1 |

8 |

528 01262 |

Return Spring |

1 |

9 |

528 01272 |

Return Spring |

5 |

10 |

639 10590 |

Pinion |

1 |

11 |

726 00092 |

Bearing |

1 |

12 |

726 00142 |

Bearing |

1 |

13 |

728 00270 |

Roller |

5 |

Source: The authors (2016)

Among the thirteen different components required to assemble the starter 1000, only four components are produced by the company. Therefore, only these were the object of the study of this work, as the other components are purchased from specialized companies and therefore do not constitute costs for the company.

The company manufactures the four components of the starter 1000 in-house, and so the appraisal costs it generates are: crown 135.0015.0, shaft 220.0074.0, pinion 639.1059.0 and roller 728.0027.0. Figure 5 shows the list with only the four components manufactured by the company and that generates appraisal costs to the same.

Figure 5 – List of the components fabricated by the company of the starter drive gear 1000

Starter Nº 1000 |

|||

List of Components |

|||

Nº |

Part code |

Part name |

Quant. |

1 |

|

|

|

2 |

|

|

|

3 |

|

|

|

4 |

|

|

|

5 |

135 00150 |

Crown |

1 |

6 |

220 00740 |

Shaft |

1 |

7 |

|

|

|

8 |

|

|

|

9 |

|

|

|

10 |

639 10590 |

Pinion |

1 |

11 |

|

|

|

12 |

|

|

|

13 |

728 00270 |

Roller |

5 |

Source: The authors (2016)

As the vast majority of the starter drive gears produced in the company, the starter 1000 must go through several manufacturing stages that are carried out in different sectors of the company, and the processing of these stages pursues the transformation of a portion of gross raw material of "steel" into various mechanical components of high precision that will be compiled in the assembly sector, thus generating the starter drive 1000.

The sectors responsible for this transformation in sequential order are: cold formation, machining, heat treatment and assembly. Despite all the sectors above are interconnected for producing the starter drive and also depend on each other because of the customer and supplier relation, each sector has different specificities regarding the costs of production, inspection, dimensional control, testing during production and appraisal costs.

As mentioned above, appraisal costs refer to the necessary inspections of the product, for it must fulfill the project requirements. It is important to remember that there are two different categories of inspection. There are those carried out during production of the item and therefore they do not increase the cycle time of production, avoiding impacts on the production cost. This category of inspection, which does not cause financial impact, is not considered a real appraisal cost since it does not appear during the process; it becomes "invisible" in front of an inquiring look covering costs. Another category is the inspection cost that extrapolates the time in the production cycle and therefore generates real impact on the cycle time and production costs. In this situation, the costs of production and the appraisal costs are obtained.

In agreement with the quality area it has been determined that for this study only the cost of the second category would be considered, that is, inspections that actually generate some impact on production cost. The objective of this study would be to facilitate the understanding of the existence and impact of appraisal costs in the production process of the starter drive and its components. Another endeavor of this study was to elaborate, in conjunction with the quality area and business costs, a worksheet that presents in a simple and feasible way all the important information on the production, manufacturing costs, and appraisal costs of each component.

It is also important to mention that the information concerning the manufacturing costs of the components presented in this study has been changed, responding a matter of security and confidentiality of the company information. However, to ensure the quality and reliability of this study all the values passed through the same "scale factor" and the percentage value of the information has been preserved and has not undergone any changes.

The worksheet for the appraisal costs calculation considers the costs in every stage of the production process of each component, and also shows the percentage of appraisal costs contribution to the manufacturing cost per component. The following is the list of the information covered by the worksheet:

a) Component name;

b) Production sector;

c) Number of stages;

d) Production stage;

e) Manufacturing cycle time on each stage per component unit in seconds (s);

f) Manufacturing cost of each stage per component unit in US Dollars ($);

g) Appraisal time per component unit in seconds (s);

h) Appraisal cost per component unit in US Dollars ($);

i) Percentage of appraisal cost in relation to the manufacturing cost (%)

j) Total manufacturing cost per component in US Dollars ($);

l) Total cost appraisal per component in US Dollars ($);

m) Percentage of the total cost appraisal in relation to the total manufacturing cost per component (%).

Below, according to Table 1, the worksheet to calculate the appraisal cost corresponding to each production stage.

Table 1 - Worksheet appraisal cost calculation

TABLE FOT THE APPRAISAL COSTS CALCULATION |

|||||

Component: |

|||||

Sector: |

|||||

Quantity of stages: |

|||||

Stage of production |

Cycle time (s) |

Manufacturing Cost ($) |

Appraisal time (s) |

Appraisal Cost ($) |

Percentage of Appraisal Cost in relation to the Manufacturing Cost |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Manufacturing Cost ($) |

0,00 |

||||

Total Cost Appraisal ($) |

0,00 |

||||

Percentage of Total Cost Appraisal in relation to the Total Manufacturing Cost (%) |

0,00 |

||||

Source: The authors (2016)

At the end of the data collection from each production stage, the information gathered was reviewed and condensed on a second worksheet that calculates the total quality appraisal cost of the starter drive 1000. It can be observed in Table 2, below:

Table 2 - Worksheet that calculates the total quality appraisal cost of the starter drive

TOTAL COST APPRAISAL OF THE STARTER DRIVE GEAR 1000 |

||||||

Product: Starter driver gear, code 1000 |

||||||

Components: 135.0015.0 / 220.0074.0 / 639.1059.0 / 728.0027.0 |

||||||

Sector: Cold Forming/Machining/Heat treatment/Assembly |

||||||

Quantity of stages: 25 |

||||||

Component |

Production Stages |

Cycle time (s) |

Manufacturing cost ($) |

appraisal time (s) |

Appraisal cost ($) |

Percentage of Appraisal Cost in relation to the Manufacturing Cost |

Crown |

Cold Forming 1 |

16,46 |

1,65 |

0,00 |

0,00 |

0,00 |

Cold Forming 2 |

21,94 |

1,31 |

0,00 |

0,00 |

0,00 |

|

Inspection 100% |

6,94 |

0,05 |

6,94 |

0,05 |

100,00 |

|

Machining 1 |

66,76 |

1,11 |

0,00 |

0,00 |

0,00 |

|

Machining 2 |

148,94 |

2,49 |

0,00 |

0,00 |

0,00 |

|

Heat Treatment |

58,18 |

2,32 |

0,00 |

0,00 |

0,00 |

|

Shaft |

Cold Forming 1 |

22,90 |

1,37 |

0,00 |

0,00 |

0,00 |

Machining 1 |

61,48 |

1,73 |

0,00 |

0,00 |

0,00 |

|

Machining 2 |

36,52 |

1,03 |

0,00 |

0,00 |

0,00 |

|

Machining 3 |

57,72 |

2,78 |

0,00 |

0,00 |

0,00 |

|

Heat Treatment |

19,94 |

0,80 |

0,00 |

0,00 |

0,00 |

|

Pinion |

Cold Forming 1 |

16,00 |

5,81 |

0,00 |

0,00 |

0,00 |

Cold Forming 2 |

13,34 |

0,80 |

0,00 |

0,00 |

0,00 |

|

Machining 1 |

13,18 |

0,37 |

0,00 |

0,00 |

0,00 |

|

Machining 2 |

24,52 |

0,69 |

0,00 |

0,00 |

0,00 |

|

Machining 3 |

10,92 |

0,31 |

3,54 |

0,01 |

3,23 |

|

Machining 4 |

18,94 |

0,53 |

0,00 |

0,00 |

0,00 |

|

Machining 5 |

96,86 |

2,71 |

13,84 |

0,04 |

1,48 |

|

Heat Treatment |

28,80 |

1,15 |

0,00 |

0,00 |

0,00 |

|

Roller |

Cold Forming 1 |

1,00 |

0,06 |

0,00 |

0,00 |

0,00 |

Machining 1 |

1,46 |

0,07 |

0,00 |

0,00 |

0,00 |

|

Heat Treatment |

1,12 |

0,04 |

0,00 |

0,00 |

0,00 |

|

Inspection 100% |

0,33 |

0,01 |

0,33 |

0,01 |

100,00 |

|

Assembly |

Assembly 1 |

224,50 |

13,72 |

0,00 |

0,00 |

0,00 |

Inspection 100% |

6,20 |

0,38 |

6,20 |

0,38 |

100,00 |

|

Inspection 200% |

28,30 |

0,20 |

28,30 |

0,20 |

100,00 |

|

|

|

|

|

|

|

|

Total Manufacturing Cost ($) |

43,49 |

|||||

Total Cost Appraisal ($) |

0,69 |

|||||

Percentage of Total Cost Appraisal in relation to the Total Manufacturing Cost (%) |

1,58 |

|||||

Source: The authors (2015)

How is it possible to observe the quality appraisal cost present in the manufacturing process of almost all sectors where the starter drive 1000 is manufactured?

Referring to the total costs; the total manufacturing cost of each starter drive 1000 unit, according to the collected data, is $43.49 USD. Regarding the total quality appraisal cost, it presented a value of $0.69 USD per unit, indicating a percentage of 1.59%.

Companies must maintain the focus of their activities on their customers; quality has become a basic obligation of the organizations and not as a strategic differentiator. The control over each product, service and process is mandatory to ensure the profitability and effectiveness of a company.

In this sense, as demonstrated by this study, it is possible to identify and measure the quality appraisal costs throughout the manufacturing process of a product, with the purpose of using this information to improve the administration and control the impacts of such costs on medium and long term. The quality costs need to be managed and controlled carefully, maintaining awareness in the organization that seeks to be profitable and competitive.

As can be seen, the quality appraisal costs is a strategic tool of great importance, able to contribute with the business of an organization, regardless of its size or field of activity, helping it to be positioned always ahead of the competition.

BAIMAN, S.; FISCHER, P. E.; RAJAN, M. V. Information, contracting and quality costs. Management Science, vol 46, issue 6, pag 776-789, 2000.

BERLINER, C.; BRIMSON, J. Gerenciamento de Custos em indústrias avançadas. SãoPaulo: T.A. Editor 1992.

CAMPO, B. R. Custos da qualidade.caderno de Administração Unigoiás-Anhanguera. Número1p.11-22, 2003.

CHIZZOTTI, A.Pesquisa qualitativa em ciências humanas e sociais 5.ed. São Paulo: Cortez, 2001.

FEIGENBAUM, A. V. Total quality control. 3. ed. ver. Singapure, Mcgraw-Hil, 1996

FREIESLEBEN, J. On the limited value of cost of quality models. Total Quality Management & business Excellence. Vol 15 – Issue 7 - pag 959-969. 2004.

GARRISON, R. H.; NOREEN, E. W. Contabilidade gerencial. São Paulo; Ltr, 2001.

GIL, A.C.Como elaborar projetos de pesquisa. ed. 4. São Paulo:Atlas 2007.

HORNGREN, C. et all. Contabilidade de Custos. Rio de Janeiro: Editora LTC, 2000.

JURAN, J. M. Juran’s quality handbook.2 ed. Ney York: McGraw-Hill, 1998.

MATTOS, J.C. Custos da qualidade como ferramenta de gestão da qualidade: conceituação, proposta de implantação e diagnóstico nas empresas com certficação ISO 9000.Disertação de Mestrado DEP/UFSCar. São Carlos, 1997.

ROTONDARO, R.Custos da Qualidade: Ferramentas para análise de Decisão Estratégica. Apostila da fundação Carlos Alberto Vanzolini, 1996.

ROBLES JUNIOR, A. Custos da qualidade: uma estratégia para a competição global.São Paulo: Atlas,1994.

SAUNDERS, M.; LEWIS, P.; THORNHILL, A. Reserch Methods for Bussiness Studentes. 6 ed. Englewood Cliffs, NJ: Prentice-Hall, 2012.

SHANK,J. K.; GOVINDARAJAN,V. A revolução dos custos. 2 ed. Rio de Janeiro: Campus, 1997.

TOLEDO, J.C.Conceitos sobre custos da qualidade:Apostila. p. 2- 14, 2002.

1. Business Administrator from the University of Center Brusque - UNIFEBE, Brusque, Brazil, e-mail: marcosmapg@hotmail.com

2. PhD of the Graduate Program in Accounting and Administration of the Regional University of Blumenau - FURB, Blumenau, Brazil, e-mail: sgripa@al.furb.br

3. Master of the Professional Master's Program in Production Engineering, University Center Sociesc - UniSociesc, Joinville, Brazil, e-mail: w.lopo@uol.com.br