1. Introduction

The study of the prices behavior in financial markets has generated much interest from researchers. The Efficient Market Hypothesis in the form of weak efficiency states that the prices behavior follows a random walk, being impossible the creation of mechanisms to obtain abnormal profits in pre-determined periods.

The investigation of abnormal returns with data within the same day and different days of the week offers further insight to understand the prices behavior in financial markets. Using intraday data can reveal new information that cannot be seen with data in another time period (APOLINARIO, SANTANA, SALES AND CARO, 2006). Thus, the possible existence of the weekday effect or intraday seasonality is evidence against the Efficient Market Hypothesis under the weak form. According to Fama (1991), share returns are unpredictable with respect to their past returns and thus cannot carry pertinent information from their past to historically preach prices formation. The efficient market inference predicts implications for investors, portfolio formation to strategies and market decisions. Capital market investors seek to identify abnormalities to realize abnormal returns by speculating in the same day or in specific days of the week.

This study aims to evaluate the weekday effects and intraday seasonality in the stock return and liquidity belonging to Bovespa index. As liquidity/illiquid measures, it is used the amount of securities, trading volume and spread. The high frequency data are obtained for each five minute interval during April and October 2009. October was analyzed until day 16th to match up to the others with respect to time, as it is the beginning of the daylight saving time on Sao Paulo stock market. The total data for each share was 11,424, with 65 shares analyzed, all belonging to Bovespa index.

The paper is structured in five sections besides this introduction. Section two concerns the review of literature on the weekday effect and intraday seasonality. Section three presents the data used and the methodological procedures applied in the research. The results are set out in the fourth section. Finally, section five presents the conclusions about the study.

2. Literature Review

2.1 Weekday effect

Fama (1991) suggests that the behavior of stock prices follows a random walk and, in this sense, it is not possible to use arbitration in order to obtain abnormal returns. Relevant information from assets would already be included in prices so, according to negotiation strategies based on past price trends, investor is unable to have higher profit on purchases based on graphs and quantitative studies than if choose to just buy and hold assets in the long term.

Guo and Tian (2007) analyzed the volatility of Shanghai Composite Stock Index, which indicates a standard ‘L’ in data series for five minute intervals, that is, the market starts with high volatility and tends to decrease until prevail certain stationary situation throughout the day. Lui and Tang (2002) analyze daily returns for 15 minutes data between Hang Seng Index (HSI) and Hang Seng Index Future (HSIF), finding increased volatility in daily market returns (HSI) for every day of the week compared to futures market (HSIF), with Mondays as the highest average return.

In studies about weekday effects, daily returns from assets of the stock market move up in different ways throughout the week, respecting the local scenario. Gibbons and Hess (1981) concluded that the average negative returns on Monday did not happen for other days of the week in the USA market, confirmed by Jaffe and Westerfield (1985), which found negative effects on Monday average returns in the United States, Canada and England stock markets and significant Tuesday negative returns in Japan and Australia stock markets. In a study with similar conclusions, Aggarwal and Rivoli (1989) observed lower mean on Monday and Tuesday returns in China, Singapore, Malaysia and the Philippines stock markets, from September 1976 until June 1988, concluding that the strong Tuesday effect is attributed to the time difference of 13 hours between New York and these markets.

The weekday effect is also found in the Brazilian market. The study by Costa Jr. (1990) applied multiple regression with dummy variables for Bovespa index daily data in the period 1986-1989 and analyzed that returns observed on Monday tend to be significantly negative, while Friday returns tend to be positive. A similar study for the Brazilian market can be found in the paper of Lemgruber, Becker and Chaves (1988) for daily closing data between 1983 and 1987 and a sharper Monday effect was identified in less negotiated shares for daily opening, closing and average data from 1986 to 1989 in the study by Costa Jr. and Lemgruber (1993). In this study, the authors recognize the possibility of heteroskedasticity in returns, but not autocorrelation, since the presence of autocorrelation may invalidate the theoretical results based on hypothesis testing, being susceptible to errors.

On the other side, Bone and Ribeiro (2002) evidenced weekday effects in nearly half Ibovespa shares using a more recent sample, from January 1996 until December 1998, White econometric tests (heteroscedasticity), Wald test (linear regression) and LM test (autocorrelation and ARCH modeling), with Tuesday the day with greater differentiation, where the average returns of half the shares surveyed were greater than Monday, a situation called as Brasilia effect by authors because results may be affected by the possible influence of Congress political information in the capital market.

Within this same point of view, considering the Latin American market, the study by Costa Jr. and Ceretta (2000) using stock market indexes from Brazil (Bovespa), Mexico (Inmex), Argentina (Merval), Peru (IGPA) and Venezuela (BBO-Index), through regression with dummy variables, found results that show the existence of the weekday effect in Peru and Venezuela, with evidence of significant differences in Monday and Friday average return, but there is no distinction between beginning and ending days of the week. A similar study is conducted by Figueiredo, Silva and Souza (2002), who studied the daily closing price of the Brazilian, Argentine and North American markets from 1995 to 2001. The technique used was multiple linear regression analysis and the authors did not find a weekday effect for BOVESPA, weekday effect (Monday (negative), Wednesday and Thursday (positive)) for Buenos Aires stock exchange and the presence of the Friday effect in Dow Jones index. On the other side, Fajardo and Pereira (2008) did not detect any abnormality in the weekday effect, holiday effect and daily seasonality for the Brazilian market, investigating Ibovespa seasonal effects using multiple regressions in the period 1995-2007.

In the evaluation of the weekday effect for daily, weekly and monthly frequencies, the study by Aguiar (2006) for the Brazilian market used regressive models for companies’ shares grouped by size and concluded that there is incidence of negative effect on Monday and positive effect on Friday in the predictability of returns. This investigation covered the period from July 1st, 1994 to June 30th, 2005.

Analyzing the daily closing values of the sessions for the weekday effect from the perspective of liquidity, volatility and financial returns in the Brazilian market between 1999 and 2006, Ceretta Vieira and Milach (2008) found low liquidity on Monday, larger quantities of businesses on Tuesday, above average returns on Wednesday, while they are below average on Thursday and is Friday is lower compared to the average on Thursday.

For a more comprehensive database study (1986-2006), analyzing Ibovespa daily average returns and specific anomalies with Monday effect, Santos, Mussa, Rêgo and Silva (2008) found evidence of the existence of this anomaly, with Monday being statistically lower than other days’ average.

Furthermore, Silva and Lima (2007) found empirical evidence of the January effect in the Brazilian stock market using data from daily closing prices of Ibovespa for the period 1994-2006. In this study, as a good specification for the regression model was not found, the authors chose to apply the following econometric models: AR (Auto Regressive), ARMA (Auto Regressive Integrated Moving Average) and GARCH (General Regressive Conditional Heteroskedasticity) and did not find January effect to monthly returns in the post Plan Real.

2.2 Intraday seasonality

Seasonality is an important factor in the predictable behavior of stock returns. Intraday effect or intraday seasonality means there are abnormal returns during the session for a specified time. The access and analysis of intraday data, also called high frequency data, provides a great potential to broaden the understanding of financial markets. Some foreign studies in finance literature, as Smirlock and Starcks (1985), Harris (1986) (1989), Jain and Joh (1988), Vijh (1988), Chan, Christie and Schultz (1995) and Pagano, Peng and Schwartz (2008) reported that intraday seasonality significantly exists in international capital markets. This implies that large profits can be earned using a simple trading rule, based on the seasonal nature of intraday stock returns, such as buying and selling stocks in a given time of the day.

In Brazil, there are few studies on intraday data. The study by Moreira and Lemgruber (2004) uses a series of Ibovespa intraday data with a 15 minute interval in the period from 04/06/1998 to 07/19/2001, totaling 803 days and 23,287 observations. The authors use these data to forecast volatility estimating GARCH and EGARCH models and VaR (Value at risk) modeling risk, making a comparison with the estimation the daily data volatility. They conclude that there is a distinction between series, where the forecast of volatility and intraday data returns can bring significant benefits related to risk management in financial markets.

Oliveira (2008) analyzes the return with high frequency data for Petrobras asset preferential type, traded at Bovespa, in order to discover the behavior of the returns conditional variance through ARCH methodology. The study includes intraday basis from January 3rd until April 13th, 2005 with 120,000 observations in 69 trading days and uses five minute intervals. In conclusion, the author emphasizes that there is a strong intraday seasonality and using APARCH model with long memory can have better results than ARCH models with short memory, highlighting their importance for the pricing of options and risk market.

Relevant papers were developed in international markets, as Harris study (1986), one of the pioneers in studying the returns in the USA stock market using intraday data. This research documents patterns in data called "U" pattern due to the intensity of negotiations during the day, which is usually higher at the opening and closing and lower during the lunch hour.

Harju and Hussain (2006) analyzed data with a 5 minute interval of the four major stock indexes in Europe, from September 1st 2000 until August 29th, 2003, totaling three years. In this study was identified that, after the USA market opening, the impact on returns and volatility in the European market is immediate and all markets respond identically, that is, there is a seasonal effect after opening the USA market in relation to the European market in which intraday patterns were affected by USA macroeconomics events. Besides, the intraday effect was observed in all European markets.

Analyzing the end of the day effect with intraday data for the USA S&P 500, Harris (1989) concludes that this is caused by an increased frequency in offer prices at the end of the day on which the closing return is positively significant. These results corroborate the Vijh study (1988), in which is reported that the frequency of the offer prices for stock market significantly increases at the end of the day. Besides, Smirlock and Starcks study (1985) for Dow Jones in the period 1963-1983 observed that Monday first hour return compared to Friday last hour is significantly positive.

Harris (1986) reports there was a general increase in New York Stock Exchange (NYSE) prices in the last business of the day between December 1st, 1981 and January 31th, 1983. One of the conclusions is that the average positive returns in equity markets tend to occur during the first 45 minutes of the session and also realizes that returns are higher near the end of the day, especially on the last business of the day.

Evidence for effects on intraday data are also verified in the study by Copeland and Jones (2000), which investigated patterns in returns, volatility and trading volume in stock index futures and the Korean market (KOSPI-200) from January 1997 to December 1998, using an intraday data sample with a five minute interval. The conclusions of this study show a significant impact on adjusted average patterns of volume and volatility, similar patterns to those found in Western markets are also highlighted in the study.

Yang and Wang (2010), using high frequency data with 30 minute intervals sought to test the futures market efficiency for the four major energy sources (crude oil, heating oil, gasoline and natural gas) for New York Mercantile Exchange (NYMEX) from December 2000 to May 2007. The analysis techniques were neural network models, semi-parametric functional coefficient models, nonparametric Kernel regression and GARCH model for nonlinear data in the forecasting context out of sample, testing together economic and statistic data. It was found evidence with significant estimates only for data on economic criteria and limited evidence for intraday market inefficiency in energy futures prices, while from the four analyzed futures markets only two markets (heating oil and natural gas) showed robust forecast evidence during the bull market condition.

Beattie and Fillion (1999) conducted a study with intraday data on exchange rates using 10 minute intervals in Canada and the United States. The authors also found seasonal patterns related to the arrival of information from other markets across estimated equations to explain the volatility in intraday seasonal patterns, daily volatility and macroeconomic news. It was found that intervention by the central bank had no direct impact on reducing Canadian dollar volatility.

The existence of intraday effects is also evaluated in other types of markets, as studies made by Muller et al. (1990) and Baillie and Bollerslev (1990) for the foreign exchange market, Aggrawal and Gruca (1993) for the options market, Cornett, Shwarz and Szakmary (1995) for the futures exchange and Jordan, Seale, Dinehart and Kenyon (1988) to study the commodities market.

3. Method

3.1 Data

The database was obtained through the software ProftChart version RT (Real Time) used to analysis the stock market. The base was exported through software by CSV command. The sample period was April 1st, 2009 to October 16th, 2009 and contains intraday transactions realized from five to five minutes, covering the 65 assets classified in Bovespa index theoretical portfolio in the period. For each asset a data series was obtained, with 11,424 observations for each share for a period of 136 days. Bovespa opening hours, at 10:00 a.m., until the normal market close, at 5:00 p.m., were considered to form intervals. However, it was observed that due to the closing auction of the Brazilian market at 4:55 p.m., there was no data for the range of 5:00 p.m. and, therefore, this interval was excluded from the sample. Holidays and weekends were not considered for returns calculation.

3.2 Statistical tests

Data analysis was performed using the analysis of panel data methodology because it confronts the pattern of the same company over time (longitudinally) and in relation to other companies (cross-section). According to Baltagi (2008), this analysis technique is one of the most innovative in the econometrics literature, demonstrating a rich environment for the developed estimation techniques and consistent theoretical results.

The main advantage that the panel data analysis has on a cross-section analysis is that it allows a great flexibility in modeling differences in individual behavior. Some studies on this subject in the international literature are Park, Sickles and Simar (1998, 2000), Hsiao, Lahiri, Lee and Pesaran (1999) and Ghysels and Osborn (2001).

Hsiao (2003) and Baltagi (2005) list a number of benefits in using panel data, such as: a) controls the individual heterogeneity of firms; b) provides more information; variability and degrees of freedom under collinearity in the data, resulting in efficiency; c) is better for the dynamic adjustment, enabled to identify and measure effects that are not easily detectable in cross-section models and d) allows to build and test more complicated behavior models than cross-section. The general model for panel data can be expressed as [1].

![]() . [1]

. [1]

where the subscript i = 1,..., k indicates the i-th firm, t = 1 ,..., T indicates the time and β's are the regression coefficients. The variables are given by: yit = dependent variable for firm i at time t; x1 = independent variable 1 for firm i at time t; xn = independent variable n for firm i at time t; eit = error term for firm i at time t.

There are three cases of analysis to fit the general model in order to make it more functional. Pooled, Fixed-Effects and Random Effects models. In the pooled model, the intercept is the same for the whole sample, that is, it is assumed that all elements of the sample have identical behavior. In the fixed-effects model there may be variation in the intercept between companies and it is most suitable in situations where the firm specific intercept can be correlated with one or more regressors. In the random effects model, it is assumed that firms for which data are available are a random extraction of a population with a constant average value.

To construct the model, first it is necessary to check whether the variables have significant linear associations. If this occurs, one may have to face the problem of multicollinearity that is verified by calculating the variance inflating factors (VIF), given by VIF(j) = 1/(1 - R(j)^2), where R(j) is the multiple correlation coefficient between variable j and the other independent variables. If the model is free of multicollinearity, the choice between models can be accomplished through specific tests.

Regarding liquidity, we used six measures according to weekday effects and intraday seasonality. On Table 1: i) spread1, ii) spread2, iii) variation in volume, iv) variation in the amount of securities, v) variation in the weighted volume and vi) variation in the amount of weighted securities. The formulation 1 properly adjusted with dummy variables was used to perform the analysis of the weekday effect and intraday seasonality.

Table 1- Variables definition

Variables |

||

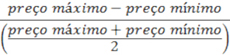

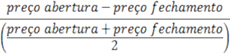

| Spread1: variation in opening and closing share prices affected in the interval |

|

|

| Spread2: variation in opening and closing share prices affected in the interval |  |

|

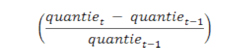

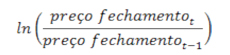

| Return: return with the closing prices of the company's stock |  |

|

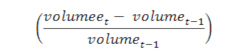

| Variation in volume: trading volume variation in company's stock, measured in Reais |  |

|

Variation in the amount of securities: variation in the amount of securities traded in the interval |

|

|

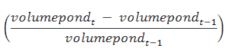

Variation in the weighed volume: variation in volume, measured in Reais, weighed by Bovespa index* |

|

|

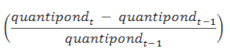

Variation in the amount of weighed securities: variation of securities negotiated in the interval, weighted by Bovespa index* |

|

|

* The purpose of weighting is analyzing the share liquidity behavior in relation to the market liquidity behavior. |

||