Hamilton Pozo*

Recibido: 10-07-2010 - Aprobado: 16-09-2010

| ABSTRACT: The aim of this article is to identify some of the main strategies related to the practical use of the Theory of Constraints (TOC) with a tooling in production management. It seeks to prove that this theory does not treat organizations as a collection of independent processes, but rather as an integrated system. A case study of the use of Theory of Constraints in a small sized company of automotive spare parts production located in the city of Campo Limpo Paulista (São Paulo) that introduced TOC and the results obtained are reductions in the lead times of their processes and reduction of stocks. Keywords: Theory of Constraints; Tooling; Production; Small Zised Company |

RESUMEN: |

The Theory of Constraints’ essential premise is that all firms have at least one critical constraint that limits their production capacity. A constraint is any element whatsoever that occurs in a system and that keeps the said system from achieving optimal performance. By using the Theory of Constraints, management can control the contribution margin and the product’s unit production cycle with regard to its critical resources, i.e., its constraints (bottlenecks), thus raising production capacity.

TOC can be used on three different levels:level 1: production management – to solve problems of bottlenecks, production scheduling and reduction of inventories;

level 2: process analysis - application based on the direct costing method, instead of traditional cost analysis, making it possible to base measures taken on the ongoing improvement of processes, system improvements and systems’ constraints that, in statistical terms, determine protective capacities, critical points and their key elements;

level 3: general application of TOC, aimed at tackling a variety of processing problems within the organization, by applying its logic in order to the identification of which factors are holding an organization back from achieving its targets, developing a solution to the problem of ongoing improvement.

As a new scientific manufacturing management methodology, TOC’s main objective is to promote an ongoing optimization of the expected performance in any organization that has a well-defined goal, by focusing management’s actions on those elements that are holding the organization back. It also pursues commitment to total quality and a perfect processing flow in order to achieve continuous productivity gains. Therefore, one can say that productivity is the act of bringing a firm closer to its goal.

Especially in the case of a manufacturing process, all the actions should converge so that the manufacturing plant advances toward its goal; in other words, toward meeting the customer's needs. It should be clear that for an industrial organization to increase its performance and its productivity and thus raise profits, the production flow should be optimized at the "factory floor" level, while stocks should also be drastically reduced, thus lowering operating expenses.

The basic principle of the Theory of Constraints (TOC) is the impossibility of running a balanced factory at 100 percent capacity. Variation in processing and material transfer times is the root cause of longer cycle times and higher inventories, which can hinder the ability to run a factory at full capacity. The challenges this basic principle by stating that variation in processing and material transfer times comes from special or assignable causes that can be eliminated through traditional quality management techniques. Even random or common-cause variation can be suppressed through lean manufacturing methods. This research gives a complete overview of the Theory of Constraints and its impact on engineering and managerial economics and illustrates the effect of variation in processing and material transfer times, and shows why this variation prevents achievement of 100 percent utilization. Describes methods for reducing variation in processing and material transfer times and methods for increasing productivity and reducing cycle times - these are useful for elevating the constraint (increasing its capacity) and reduce variation. How to identify and remove variations and maximize capacity to achieve bottom-line results.

The process of ongoing improvement begins with a clear definition of the organization’s goal, as well as the establishment of performance measurement parameters that are directly related to this goal. In the case of the private sector, the goal of obtaining profits goes hand in hand with a number of conditions such as quality, price and customer service, among others. These conditions must be satisfied, in the sense of achieving ongoing improvement. Therefore, the organization must use "straight-forward and ordinary" language, thus avoiding the frequent communication problems that exist in the business environment. Under a conventional system, evaluating the performance of a manager means checking to see whether or not he achieved the firm’s objective. It is necessary to evaluate the result at the end of the period in terms of the following factors; production achieved, net profit, cash flow and return on investment, along with other such items. However, this is only done afterwards. TOC provides a tool for evaluating the result of the process before, during and after it runs (Goldratt; Cox, 1987, 1988, 1989). Using intermediate indicators allows for synchronized and conscious manufacturing. The indicators suggested are as follows: value added (VA) or throughput, inventory (I), and operating expenses (OE).

Value added is defined as the speed with which the system generates financial resources through sales. Inventory represents all the financial resources spent on purchasing production inputs that will be transformed into product. In addition, operating expenses are all the financial resources necessary to turn the materials (I) into throughput (VA). Manufacturing management must keep a market oriented approach in mind, because profits come from the value added produced by sales rather than from the size of the inventory or the plant’s performance (Wooldrige; Jennings, 1995). Therefore, in order for a manufacturing process to increase its productivity, it needs to reduce inventory levels and make production more flexible by using a linear flow and avoiding interruptions to the production process. According to (Goldratt, 2003), the organization will improve its overall performance through the performance of manufacturing with regard to its productivity objectives, the performance of which will be measure by net profit, return on investment, productivity and cash flow.

Given the measures, as was explained earlier on, the firm’ s personnel can take local decisions, examining the effect of those decisions on the global processing of the production flow and on the reduction of corporate stock levels, with a reduction of the firm’ s operating expenses, resulting in an optimized decision for the business as a whole. The need for immediate availability and the value of these tools have became important factors in the performance of production areas and, consequently, in the global competitiveness of firms (Shingo, 1987; Plute, 2002; Black, 1991; Tooney, 1996, Luh, Chihchin Pan and Chihchin Wei, 2008). TOC greatly reduces business costs. This becomes clear when the theory’s assumptions are compared to the application of the principles of cost accounting (mainly the distribution of costs in order to make decisions at the local level), which leads to inadequate management decisions, both in relation to departments and in the context of the organization’s higher levels. Indeed, TOC virtually eliminates the use of Economic Order Quantities (EOQ) and production lots (Goldratt; Cox, 2002).

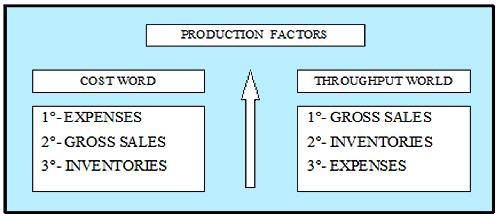

An increase in the flow, as defined, means simultaneously increasing net profit, return on investment and cash flow. A similar result is observed in terms of the drop in operating expenses. In this case, production costs are reduced while both the sales flow of products and stock levels remain constant. A reduction in inventory levels has a direct impact on return on investment and cash flow. It is necessary for the performance of the organizational processes to be measured always, or at least evaluated, so that one may have continuous improvement (Drucker, 1988). In terms of its concepts, the TOC is in the opposite of traditional cost accounting. In figure 1, we have an illustration of a comparison between conventional cost accounting and costs measured by means of throughput accounting.

Figure 1. Conventional cost accounting and accounting for costs by means of throughput

Source: Authors’ adaptation.

TOC, like Cost Accounting, regards firms as a sequence of events. Cost accounting, however, tries to reduce costs in all of a firm’s productive segments. On the other hand, TOC, which concentrates on the world of throughput, maintains its focus, concentrating almost exclusively on the firm’s critical resources. The theory is based on the premise that every firm has at least one critical constraint that limits its production capacity. By controlling constraints, manufacturing management controls the contribution margin and the product’s unit production cycle with regard to its critical resources (bottlenecks), altering its capacity. According to (Goldratt and Cox, 2002), there are two types of critical constraints: physical and political.

Likewise, one can say that to generate an increase in production or in profits one must locate the system’s Critical Constraint (incentives), in such way that the constraint changes, becoming just another "barrier" (machine capacity). Now it is no longer convenient to continue to intervene in the initial barrier, because this new obstacle becomes the system’s key determinant. In this sense, any effort in a different sequence would be a waste of time and money, since the firm will not achieve its goal.

As explained above, manufacturing is a chain of events or processes and the sequence of this chain implies in the existence and combination of two phenomena. One is called dependent events whereas the other is known as statistical fluctuations. In order to obtain an ongoing improvement in the case of physical constraints, TOC establishes a five-step Decision Process (Goldratt; Cox, 2002):

step 1: identifying the process constraints – identifying those resources whose productive capacity restricts the system’s capacity to meet its product sales flow (the constraint can even be the demand from the market itself);

step 2: exploiting the process constraints – this means getting the most out of them, for instance, not wasting time on machine bottlenecks;

step 3: subordinating everything else to the decisions that regard the constraints - the bottlenecks define the flow of production and the stocks, the use of non-bottleneck resource, among others;

step 4: relaxing the constraint – this means increasing the production capacity of the bottleneck, in the sense of increasing the system’s flow capacity;

step 5: if in step 4 a constraint was relaxed, go back to step 1 to identify the system’s next constraint.

Before applying the previously described Decision Process, some precautions should be taken first (Goldratt; Cox, 2002):

It is vital to choose a leader for the process, someone who is in a senior management position, in order to be able to alter certain high-level policies (which may characterize constraints on the system); this person should be totally committed to the firm’s Goal.

There are simple ways to identify the physical constraints and to analyze them in relation to the market’s real demand. Physical constraints can include the following: manufacturing constraints, equipment constraints, raw material constraints, input constraints, staff constraints, process constraints, and similar elements

Not everything needs to be changed; most things are good enough as they are or, alternatively, the profit resulting from changing them does not justify the cost.

Often it is obvious that a process needs to be changed, but it is unclear why it should be changed.

Even if one knows exactly what to change and why this should be changed, one still faces the difficult task of getting the firm to fully implement the change.

However, an even greater difficulty is how to answer these questions, how to treat them and how to encourage them. Moreover, in order to be able to answer these questions in a continually developing environment, it is crucial that certain skills be used as resources enabling one to identify, to find and to induce.

Identifying the key problems of each constraint is quick, to some extent, and the solution seems very viable. At the same time, these key problems can be very well hidden, sometimes even by the interested parties themselves. The firm must be able to systematically identify the "root" and not waste time on the "leaves."

Finding practical and simple solutions is essential. Complex solutions are generally not the answer. Simple solutions, on the other hand, can lead to the right solution. The motto should be: find the simple solution rather than the easy one.

Inducing the right people to come up with a good solution is the ideal way, especially when it involves changes in the basic assumptions. It is naive to expect people to embrace it, even if it seems that it has met with no resistance, because they will not understand it in the way it must be understood for its proper implementation. The only easy and practical way to overcome these obstacles is to encourage the people who will be involved in the implementation of the change to come up with the solutions "by themselves".

Once the key skills have been developed, it becomes necessary to eliminate policy constraints. To do this, the basic five-step, three-question TOC technique is applied, as is explained below.

1. Effect - cause – effect (What needs to change?)

This technique is neither new nor sophisticated, and its use allows people to get to the core problem quickly. It consists of identifying the root problems, by certifying the cause at each step.

2. Evaporating clouds

This is a technique for generating second order solutions, i.e., simple and effective solutions that produce excellent results. If a major problem can be regarded as a cloud, this technique allows us, instead of solving the problem, to make it disappear, by finding the most imperfect assumption. In other words, when the problem is major, what one should do is look for the main thing wrong with the system, making the problem disappear, just as wind carries clouds elsewhere. Smaller problems will appear, which are simpler to resolve.

3. Future reality tree (Why change?)

This is a technique for evaluating the chosen solution, finding the possible contingencies and neutralizing them, as necessary, before they occur.

4. The Prerequisite Tree

This is a technique for identifying and listing the obstacles to the implementation of the new solution, given that, with each solution, we get a new reality.

5. Transition Trees

This is the final technique, and it is the one that gives us the strategy that will enable us to implement successfully the solution obtained. The economic necessities and expected benefits are quantified at this stage. It also serves as a route map and a checklist, since it contains the sequence of quantitative and qualitative aspects expected from the solution. This tree can easily be converted into a Gantt Graph or a traditional Implementation Plan.

* Faculdade Campo Limpo Paulista - SP-BR – E-mail: h.pozo@faccamp.br

Vol. 32 (2) 2011

[Índice]